Read about our detailed, wide-ranging review and how it has resulted in measures which will protect some of the most vulnerable consumers.

Our high-cost credit review has been a detailed, wide-ranging review, resulting in measures designed to protect some of the most vulnerable consumers of financial services. The review has led to interventions for home-collected credit, catalogue credit and store cards, rent-to-own (RTO), buy now pay later offers (BNPL), and overdrafts. Recognising that high-cost credit is not the right answer for some consumers, we also want to promote the availability and the provision of alternatives to high-cost credit.

Home-collected credit

Some forms of refinancing in the home-collected credit market were more expensive than a new loan. Our analysis showed that there was harm because 55% of customers took longer to pay off than the original repayment term. This extended period mainly reflected consumers taking out additional borrowing. In 2015-17, 74% of home-collected credit consumers spent up to 12 months in continuous debt and around 10% had 12 or more loans.

Our remedies

Our changes, which came into force in March 2019, ensure any discussion on repeat borrowing in the home is consumer-led, and helps consumers fully understand their options. These changes were designed to improve sales practices, reduce hidden costs to consumers, and enhance protection against harmful repeat borrowing. We estimate that consumers will benefit from a lower cost of credit of between £4m and £34m per year.

Catalogue credit and store cards

In 2016, 14.7% of UK adults had outstanding debt on catalogue credit, and 3.7% on store cards. Some debt charities reported that catalogue credit accounted for a third of their clients. We saw harm from the cost of borrowing by this vulnerable group with median income below the national average. Similar to our work on credit cards, we found a general lack of understanding of the fees and problems with persistent debt.

Our remedies

Our rules on catalogue credit and store cards, which came into force between December 2018 and June 2019, require firms to provide customers with reminders towards the end of offer periods, tighten rules on credit limit increases, and introduce stronger protection for consumers with longer-term debt. These remedies were informed by the work we did on the Credit Card Market Study. As a result of our intervention, we expect that consumers currently in persistent debt will benefit from lower interest and charges of £134m-£317m. In addition, we also expect consumers to benefit from lower interest and charges of between £15m and £35m each year from our overall package of remedies.

Rent-to-own (RTO)

We have been tackling issues in the RTO market since we began regulating consumer credit in 2014. We have seen clear evidence of RTO users’ vulnerability. They are among the least creditworthy users of high-cost credit. Only a third are in work and most have low incomes. RTO customers focus on weekly payments more than the total cost of credit.

The harm in this market affects consumers who need to be protected from high prices which mean they can pay several times more than other people for goods. In some cases, RTO consumers were paying more than 4 times the retail price of some goods.

Work that we have done in the RTO market to make sure that firms improve the way they assess affordability and deal with consumers in financial difficulty has resulted in redress for around 340,000 consumers of RTO firms, totalling nearly £16m.

Our remedies

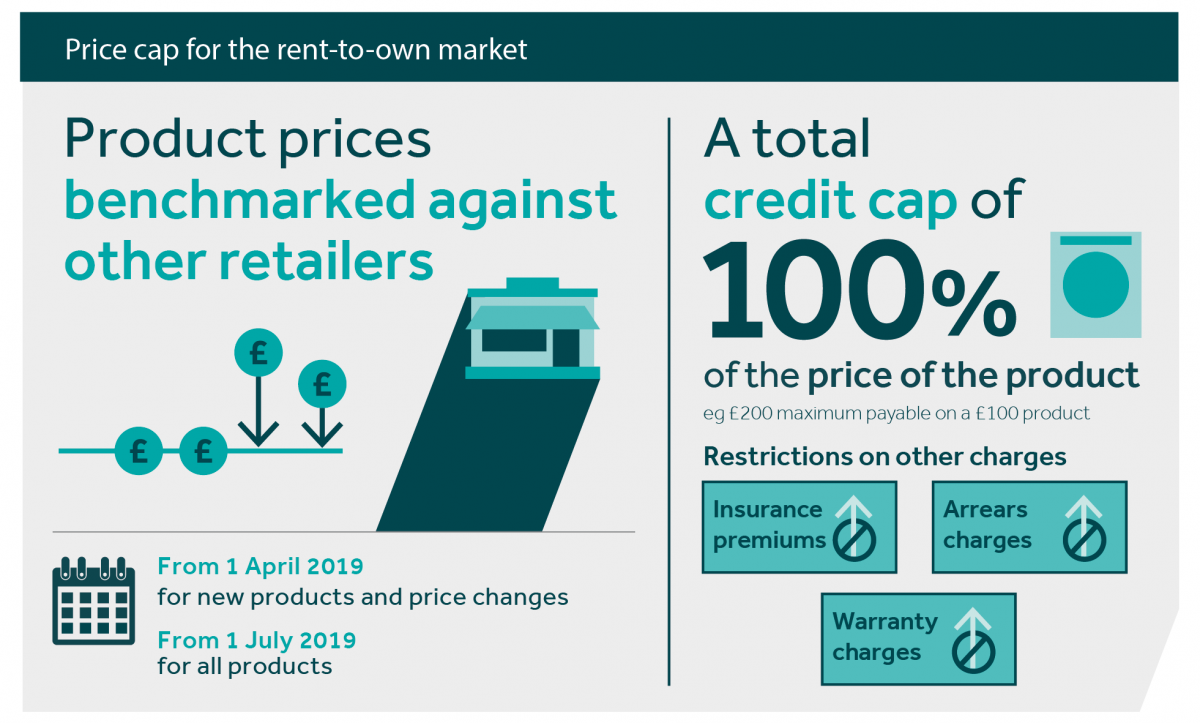

RTO price cap and improved transparency

In March 2019, we announced a price cap on RTO, which was in force for most products by 1 July 2019. The cap on these products controls prices by limiting both the cost of the product and the charge for credit. Under the cap, credit charges cannot be more than the cost of the product. RTO firms are also required to benchmark the cost of products against the prices charged by three mainstream retailers.

These rules also stop firms from increasing their prices for insurance premiums, extended warranties or arrears charges as a way of recouping lost revenue from the price cap.

The impact of our changes

We estimate that our price cap could deliver net consumer benefits of between £20m and £23m a year. We will review the impact of the price cap in April 2020.

Under our new rules, RTO firms also need to be more transparent when they show the cash value of goods, the amount of interest to be paid, and the total cost to customers.

Point-of-sale ban on extended warranties

In addition to our price cap, we also imposed a point-of-sale ban on extended warranties being sold alongside an RTO agreement. This gives consumers more time to decide if they want these additional services and took effect from February 2019. We expect this remedy to lead to net benefits to consumers of £3m-£8m per year, considering lower expenditure on extended warranty policies but also a partial loss of benefits from repairs and replacements.

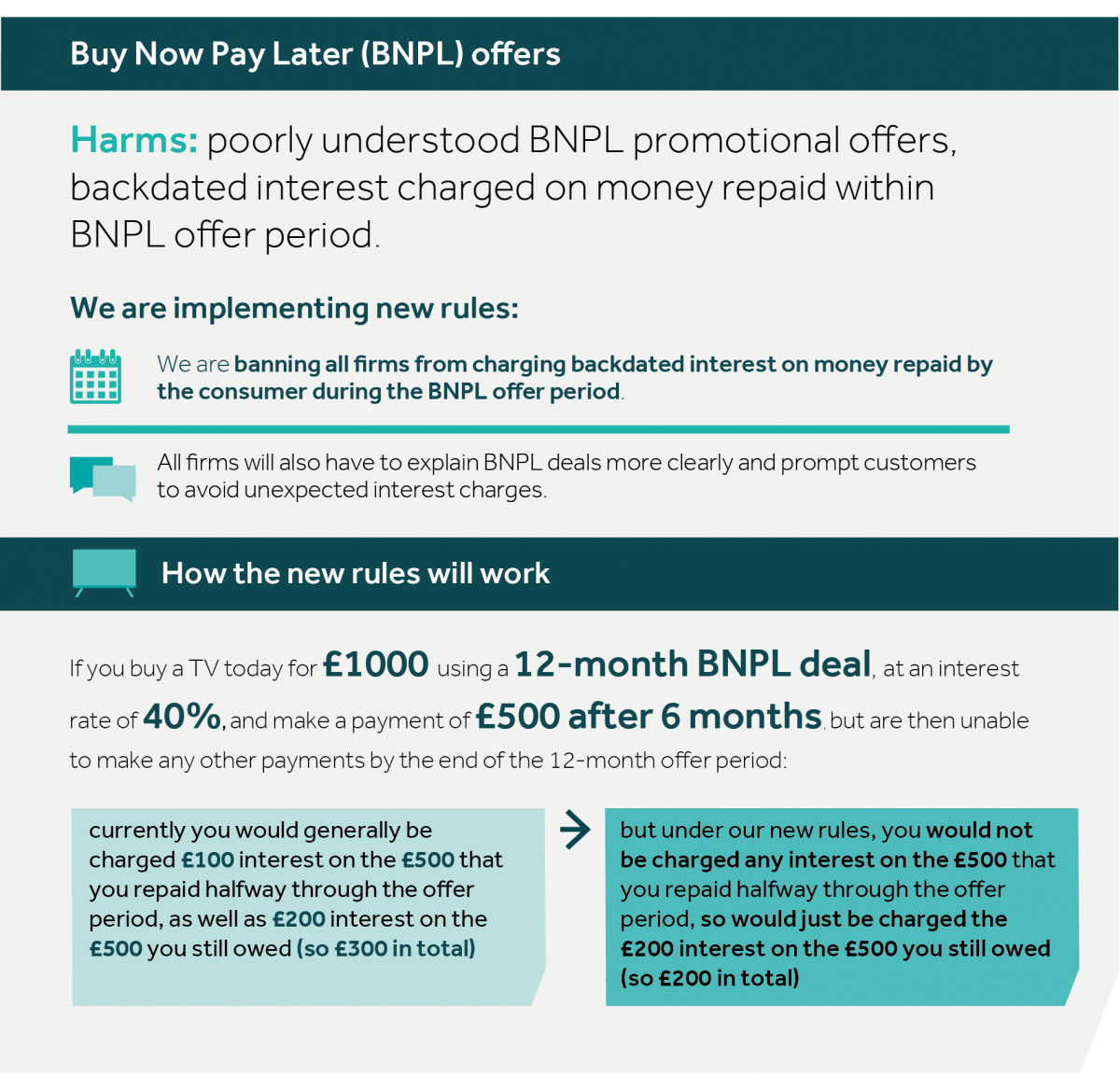

Buy now pay later (BNPL) offers

A range of firms offer BNPL as part of their credit offers; these include catalogue credit, store cards and retailers who offer finance at the point of sale.

BNPL offers tend to provide a promotional period, typically up to 12 months, during which consumers don’t have to make payments and are not charged interest. But if they don’t repay the entire amount within this period, they are usually charged interest from the date of purchase.

Consumers experience harm because the complexity of these offers is not well understood. Consumers who repay part but not all the amount owed are still charged backdated interest on that part. Typically, over a third of consumers do not repay within the offer period, incurring interest charged from the date of purchase.

Our remedies

Our new rules require firms, from September 2019, to provide better information to customers, and from November 2019 firms will be prevented from charging backdated interest on sums that customers repay during the offer period.

We estimate that these rules will save consumers around £41m-£74m per year.

Overdrafts

We identified harm to consumers, particularly to vulnerable consumers, from the disproportionate burden of high charges and the repeat use of overdrafts. In 2016, more than 50% of firms’ unarranged overdraft fees came from just 1.5% of customers. People living in deprived neighbourhoods are more likely to incur these fees.

Our remedies: The biggest intervention in the overdraft market for a generation

In June 2019, we put in place reforms to fix the dysfunctional overdraft market. These changes will make overdrafts simpler, fairer and easier to manage, and will protect the millions of consumers that use overdrafts, particularly more vulnerable consumers.

Our new rules reform the ways banks and building societies charge for overdrafts. The changes are significant and wide-ranging and have been informed by the results of our Strategic Review of Retail Banking Business Models.

The package of remedies includes:

- stopping firms from charging higher prices when customers use an unarranged overdraft rather than an arranged one

- banning most fixed fees for borrowing through an overdraft

- simplifying overdraft pricing – ensuring the price for each overdraft will be a simple, single, annual interest rate – no fixed daily or monthly charges

- requiring firms to advertise arranged overdraft prices in a standard way, including an APR

- issuing new guidance to reiterate that refused payment fees should reasonably correspond to the costs of refusing payments

- requiring banks to do more to identify customers who are showing signs of financial strain or are in financial difficulty

Better outcomes for all consumers

We indicatively estimated that the 30% of personal current account consumers living in the most deprived neighbourhoods in the UK could see an aggregate reduction in overdraft charges of around £101m per year. Additionally, pricing through a single interest rate and APR disclosure will enhance price competition, which we expect will lead to better outcomes for all consumers in the longer run.

The pricing remedies above complement and work alongside a set of competition remedies, finalised in December 2018, which aim to improve consumers’ low levels of awareness and engagement with overdrafts. The competition remedies require firms to:

- provide online tools that indicate eligibility for overdrafts

- improve the visibility and content of key general information about overdrafts, particularly when opening a new current account or requesting a new overdraft

- automatically enrol customers into a set of overdraft alerts to address unexpected overdraft use

- remove any available overdraft from the description of a customer’s available funds

Firms will be required to publish more detailed information on the pricing of their overdrafts alongside quarterly current account services information.

We estimate that consumers may save between £59m and £160m in reduced overdraft and refused payment fees and charges, as our alerts will result in them incurring these less frequently.

We want to stimulate competition by making it clear to consumers how overdrafts work, what they cost, and how much consumers are using them. Increased competition between firms may reduce prices and increase service quality. We want to ensure that charges are not unexpected and make consumers feel in control of their borrowing.

Next steps

The repeat use remedies and the competition remedies come into force on 18 December 2019, followed by the pricing rules on 6 April 2020.

We will evaluate the impact of our remedies once they have been in force for 12 months.