Read more information on the details of our price cap for high-cost short-term credit loans.

In December 2013, Parliament gave us a duty to introduce a price cap to protect consumers from excessive charges from high-cost short-term credit (HCSTC). The harm included rates that were then as high as 4% per day with a typical customer taking out 6 loans per year.

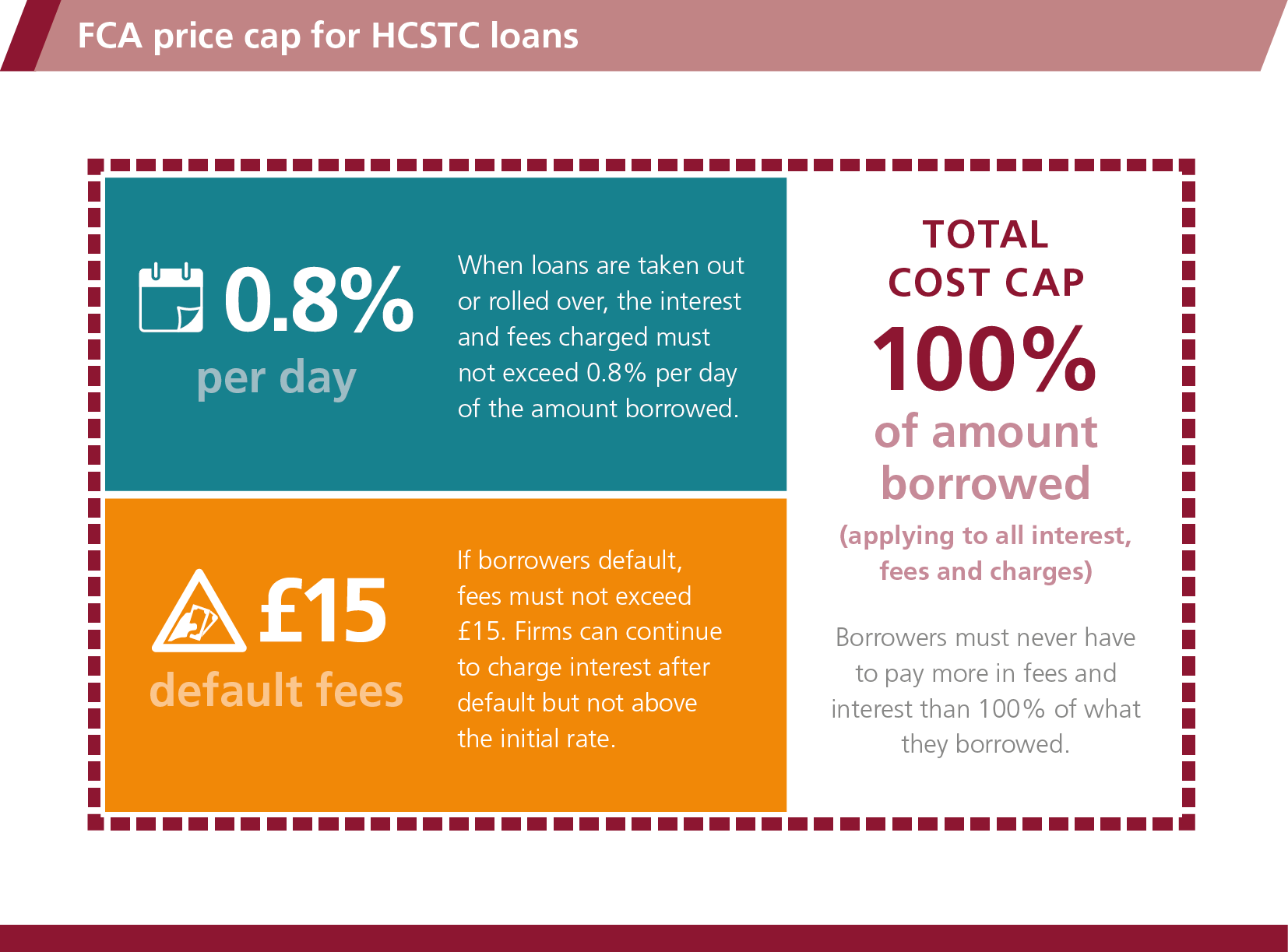

Our remedies: A price cap, risk warnings and restrictions

We introduced a price cap with effect from 2 January 2015. This followed the introduction of risk warnings to consumers and restrictions on rollovers and how recurring payments are collected.

The impact of our changes

We reviewed our HCSTC rules in 2017. We found that the 760,000 borrowers in this market have saved around £150m per year. Our reforms have led to cheaper loans, better affordability assessments, and fewer customers experiencing debt problems with payday loans. Following that review, we decided to maintain the existing level of the cap.

We recognise the role of HCSTC in supporting consumers’ short-term financial needs, and we are reviewing the price cap. We have now completed a series of round table discussions, where we engaged with firms offering HCSTC, trade associations and consumer groups, with broad stakeholder preference to retain the current cap for appropriate consumer protection and stability while acknowledging trade-offs with access. We are considering the findings but currently see no evidence for change. We hope to conclude our work shortly.