Find out we have taken measures to improve this market for those potentially in problematic debt.

In July 2016, we published the final findings from our Credit Card Market Study (CCMS), which analysed 34m customers’ account activity across a five-year period. We found that competition was working fairly well for most consumers but we had significant concerns about the scale of harm from problem credit card debt.

Remedies to make the market work better

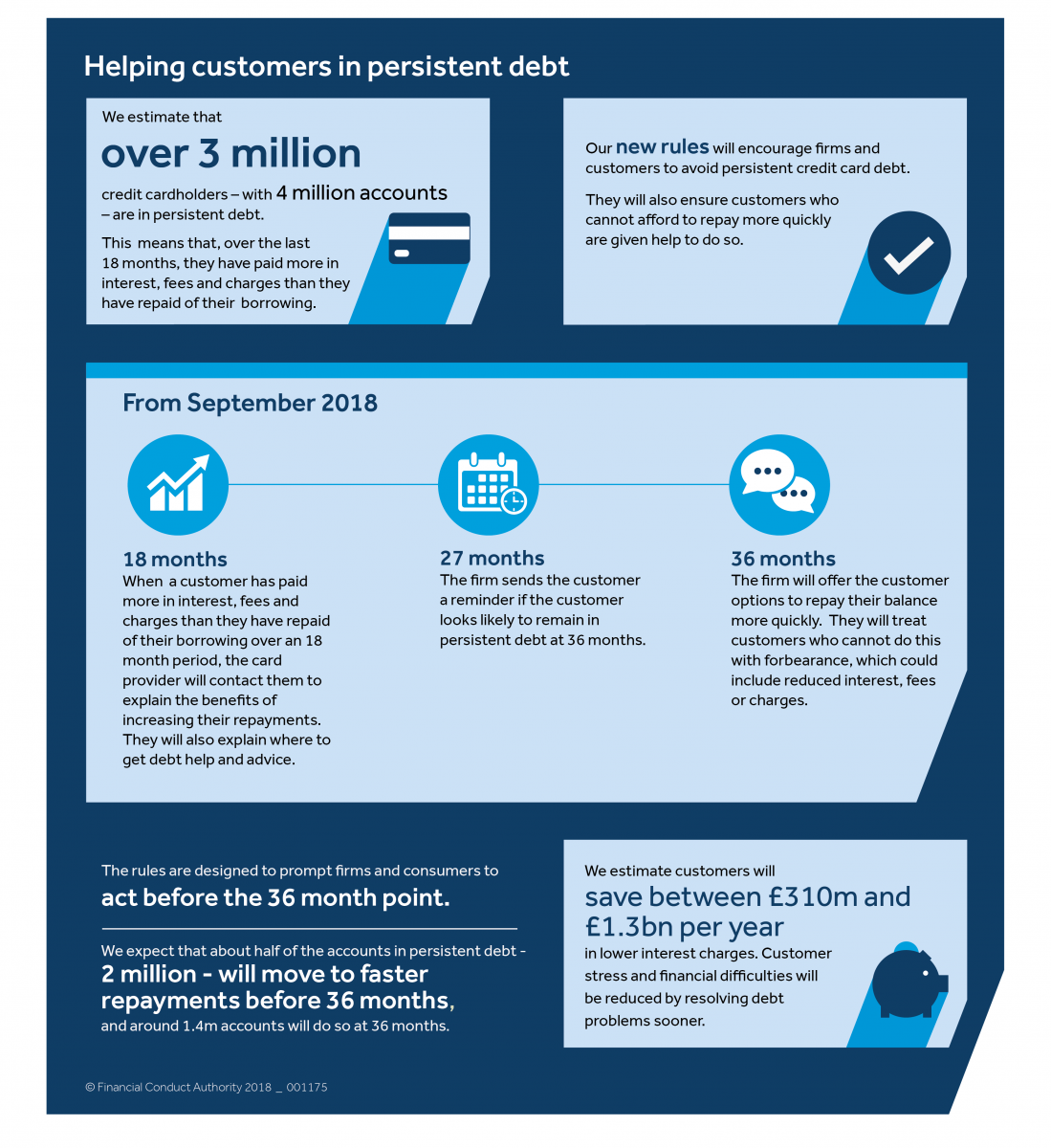

We introduced a package of remedies to give consumers greater control of their borrowing. Since 1 September 2018, firms need to identify customers in persistent debt, prompt them to change their repayment behaviour, put repayment plans in place where these prompts do not work, and intervene earlier to help customers showing signs of actual or possible financial difficulties.

Some remedies were agreed with the industry on a voluntary basis, including notifications when promotional offers are coming to an end, alerts on credit limit utilisation, and giving customers greater control over credit limit increases.

The impact of our changes

We expect these measures to save over 3 million credit card customers up to £1.3 billion per year.

What we are doing now

We are now working on the final part of the CCMS remedy package; looking at ways to encourage customers who are making low repayments to repay more when they can afford it.

We are monitoring the impact of our rules and the industry voluntary measures. We will review the effectiveness of the remedies when they have been in operation for long enough to assess consumer outcomes. We expect this to be in 2022-23.

Voluntary remedies

The Lending Standards Board has published a report on their review of the effectiveness of the voluntary remedies we agreed with the industry.

These voluntary remedies relate to notifications when promotional offers are coming to an end, alerts on credit limit utilisation, allowing customers to request a ‘later than’ payment date and giving customers greater control over credit limit increases.

The report assesses how these remedies have impacted customers’ use of their credit cards.