Read about the action we have taken to protect consumers since we took on the regulation of consumer credit in 2014.

We act to ensure markets work well, to protect consumers and to make sure they have access to the financial services they need.

Consumer credit enables consumers to buy goods and services, spreading repayments over time, and to manage cash-flow shortages.

The sector is made up of:

- credit products such as credit cards, personal loans, retail and motor finance

- high-cost credit such as high-cost short-term credit (including payday loans), home-collected credit, rent-to-own (RTO), buy now pay later offers, overdrafts, guarantor and logbook loans

- services such as debt collection, debt advice, credit information and credit broking

Borrowing is a necessity for many consumers and some do not consider its longer-term cost. This makes consumers susceptible to being sold unsuitable or poor value products and services. These concerns are more pronounced for high-cost credit users, who are more likely to be vulnerable.

In 2017, around 39m people in the UK had outstanding credit borrowing with 3.1m consumers using high-cost credit products. Consumers had £3.9bn of debt on high-cost credit products excluding overdrafts and retail finance, in January 2018. Consumers also owed £11.3bn in retail finance debt; some of this is high-cost and it mainly comprises store cards, mail order and running account credit. In May 2019, consumers had £7.7bn in overdraft debt.

What we have done and are doing in this sector

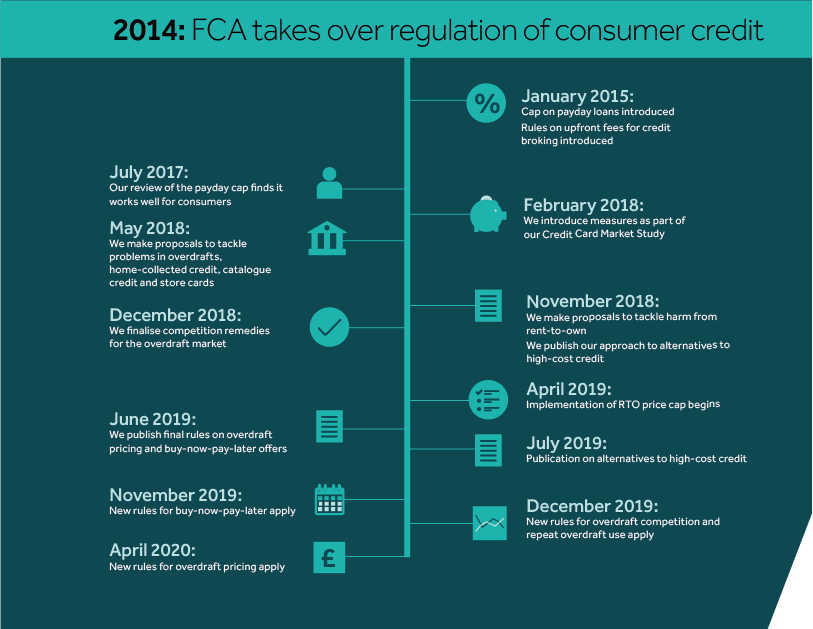

Since we took on the regulation of consumer credit in 2014, we have intervened where we have found problems.

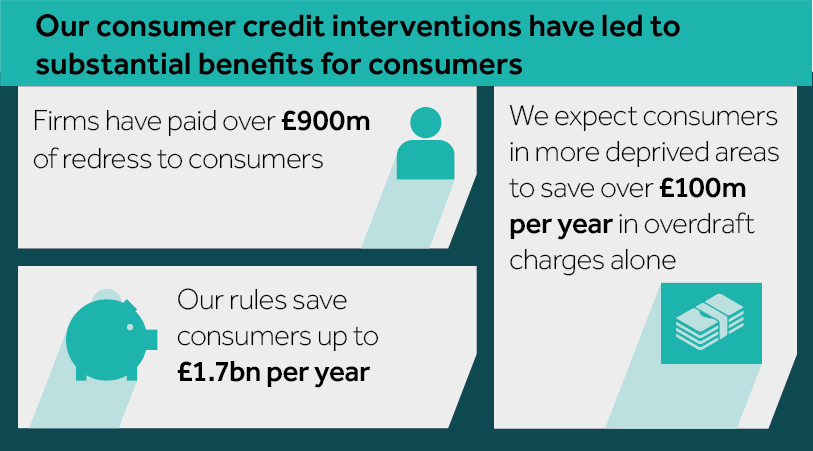

Our interventions have resulted in more than £900m in redress for consumers. Our price cap for high-cost short-term credit has already saved consumers around £150m per year. We expect our rules to save credit card customers up to £1.3bn per year. We also estimate that our overdraft alerts will save overdraft users up to £160m per year, and that our interventions will save rent-to-own users up to £31m per year and buy now pay later customers up to £74m per year.

Timeline of our policy interventions

You can find out more information by clicking on the month.

Our approach to consumer credit regulation

In 2014, nearly 50,000 firms registered with us for interim permissions. Some firms did not meet our standards and were refused full authorisation. Others chose not to go on to apply for full authorisation or found that they did not need it following Government changes to the exemptions.

We currently regulate 38,000 consumer credit firms. Over the last 5 years we have seen that many firms have fundamentally improved their business models. Generally, firms are now more aware of our expectations and act on them.

We intervene where we see harm and have the evidence that markets are not working well for consumers. We promote competition and innovation by encouraging new business models that better serve consumers, and addressing barriers that prevent markets from working as well as they could.

We authorise, supervise and enforce against our rules. We prioritise harm that affects customers who are vulnerable. We have taken action where firms have not met our rules, such as failing to properly assess creditworthiness and not treating customers fairly. Where firms in this sector have not met our expectations, this has resulted in more than £900m of redress for consumers.

Across the sector, we have found common themes of complex product design and pricing, persistent debt, and a lack of timely, clear and easily actionable information. Unaffordable lending and borrowing can cause real harm to individuals and society.

There are significant differences in how the various products operate and in how they are bought and sold. Our work has shown that the causes and drivers of harms to consumers can differ significantly between products. No single solution would give consumers the protection they need across consumer credit products.

We will continue to look at areas where we believe there may be harm. We talk about some of these areas in the section on our ongoing work.

The following pages summarise the work we have done in this sector which includes:

- High-cost short-term credit

- Credit broking, debt management and price comparison websites

- Credit Card Market Study

- High-cost credit review (covering home collected credit, catalogue credit, store cards, rent-to-own products, buy-now-pay-later offers, and overdrafts)

- Creditworthiness

- Motor finance

- Credit Information Market Study

- Guarantor loans

- Review of Consumer Credit Act provisions

- Alternatives to high-cost credit

- Our ongoing work in the sector