We set out our view of consumer harm in this market and our 3-year strategy to address this.

Our 2021/22 Business Plan set out our consumer priorities for the year ahead. One of these priorities is to enable consumers to make effective investment decisions. In early 2022, we will publish our consumer strategy to set out our ambition for this market. Ahead of that, we are publishing more detail on our consumer investments strategy to explain the work we will be doing to ensure consumers can invest with confidence. We have set ambitious outcomes for this work, and we will publish metrics to be transparent about whether we are meeting these.

To inform this strategy we’ve analysed responses to our Call for Input on the Consumer Investments Market and supplemented these with our own data and intelligence. We’ve built the strategy from our evidence base, including the evidence from our regulatory activities published alongside this Strategy in the second Consumer Investments Data Review.

1. Our aim

We want to see a consumer investment market in which consumers can invest with confidence, understanding the risks they are taking and the regulatory protections provided.

We do not want to restrict consumers if they want to invest, but we do want them to be able to access and identify investments that suit their circumstances and attitude to risk. Key to this is ensuring that consumers can get the advice or support they need, that they only access higher risk investments knowingly and that they are protected from scams.

When things go wrong, as they sometimes will, we want consumers to know how to seek compensation and for the cost of redress to be met by firms in a fairer and more sustainable way.

Infographic 1: Creating the right environment for consumers to invest

View accessible version of infographic (PDF)

Actions we will take

Table 1: actions over the next three years and outcomes at a glance

|

Mainstream investments |

Higher risk investments |

Scams and fraud |

Consumer redress |

|---|---|---|---|

|

|

|

|

|

Outcome |

Outcome |

Outcome |

Outcome |

|

20% reduction in the number of consumers with higher risk tolerance holding over £10k in cash by 2025

|

50% reduction in the number of consumers investing in HRIs who indicate a low risk tolerance or demonstrate the characteristics of vulnerability by 2025 |

Seek to reduce the amount of money consumers lose to investment scams, through reductions in investment scams perpetrated or facilitated by regulated firms |

Act to stabilise the LDII and Investment Provision funding classes by 2025, and target a year on year reduction in these classes from 2025 to 2030 |

2. Introduction

2.1. The consumer investment market today

To understand why we have developed this consumer investment strategy, it is important to have a clear idea of what the market looks like today.

Infographic 2: The consumer investments market at a glance

2.2. The consumer experience today

Long-term social and economic changes have made the consumer investment market more important than ever. Consumers are increasingly responsible for making complex decisions about their financial future, including whether and how they invest. They have a greater choice of investment products and services than ever before. Increased choice has many benefits, but this complexity increases the risk of things going wrong. So, while most of the consumer investment market meets the goals of retail investors, there are some areas where consumer harm is occurring.

- Consumers are losing significant sums of money to investment fraud and scams. 23,378 consumers reported they lost an estimated £569m to investment fraud from April 2020 to March 2021 - an almost threefold increase since 2018. On average, consumers lost over £24,000 each.

- Consumers are looking for help in avoiding scams or dealing with their consequences. We receive approximately 1,400 calls a month related to investment scams. This is double the amount we received in 2016/17 and 23% higher than in 2019. In addition, over 10,000 people visit our ScamSmart site per month on average.

- Many consumers who might gain from investing currently hold their savings in cash. There are 15.6 million UK adults with investible assets of £10,000 or more. Of these, 37% hold their assets entirely in cash, and a further 18% hold more than 75% in cash (Financial Lives Survey - FLS). Over time, these consumers are at risk of having the purchasing power of their money eroded by inflation.

- Other consumers are investing in higher risk investments, many without realising the risks. 6% of investors increased their holdings of higher risk investments during the pandemic (FLS). Yet research conducted for the FCA revealed that there is a lack of awareness of the risks associated with investing, with 45% of non-advised investors failing to recognise that ‘losing some money’ was a risk of investing.

- The characteristics of investors are changing, as well as the way they invest. Younger people are twice as likely to have invested in higher risk investments than adults overall. For example, 44% of cryptocurrencies and 31% of crowdfunding investments are held by people under 34 (FLS). In addition, there is a new, younger, more diverse group of consumers getting involved in higher risk investments. Nearly two thirds (59%) of whom claim a significant investment loss would have a fundamental impact on their current or future lifestyle (BritainThinks).

- Financial advice is not reaching all parts of the market. Half of UK adults with £10,000 or more of investible assets (around 8.4 million people) did not receive any formal support to help them make investment decisions over the last 12 months (RDR / FAMR Evaluation). Moreover, only 8% of UK adults received financial advice and only 1.3% of adults made use of online robo-advice.

2.3. Our vision for consumer investments

Like other public bodies, we are rightly accountable for our work to protect consumers. In building this strategy we have sought to address the key areas of consumer harm and set measurable outcomes, so we can track our progress.

Table 2: our vision and outcomes at a glance

|

|

Mainstream investments |

Higher risk investments |

Scams and fraud |

Consumer redress

|

|---|---|---|---|---|

|

Problem |

Some consumers who have an appetite to invest long-term are failing to consider the opportunities from investing, missing out on potential financial gains |

Consumers are losing money because they are straying (too heavily) into investments that do not meet their needs or exceed their risk tolerance, including HRIs

|

Consumers are losing money to investment scams, which in turn impacts market confidence and willingness to invest |

The cost and impact of poor advice is too high and borne by consumers or passed to other firms through the FSCS levy |

|

Harm |

8.6 million consumers hold over £10k investable assets in cash, half could potentially benefit from investing |

6% of adults were invested in HRIs during the pandemic. New investors were more likely to be young and BAME

|

£570m lost to investment fraud in 2020/21 (tripled since 2018) |

£833m FSCS bill forecast for 2021/22, 72% for consumer investments |

|

Vision |

Consumers can invest with confidence, understanding the risks they are taking and the regulatory protections provided. They can access and identify investments that suit their circumstances and attitude to risk, only access higher risk investments knowingly and are protected from scams. Should they want advice or support to invest, they are able to get it.

|

It is clear to consumers what happens if things go wrong and the cost of redress is met in a fair and sustainable way |

||

|

Outcome |

20% reduction in the number of consumers with higher risk tolerance holding over £10k in cash

|

50% reduction in the number of consumers investing in HRIs who indicate a low risk tolerance or demonstrate the characteristics of vulnerability by 2025

|

Seek to reduce the amount of money consumers lose to investment scams, through reductions in investment scams perpetrated or facilitated by regulated firm |

Act to stabilise the LDII and Investment Provision funding classes by 2025, and target a year on year reduction in these classes from 2025 to 2030

|

3. Mainstream investments

3.1. What’s driving harm in the mainstream investment market

Several factors indicate this market is not providing mass market consumers the support they need.

Our recent Evaluation of the impact of the RDR and FAMR found that among consumers with more than £10,000 of investible assets, 55% held the majority (75%) or all of this in cash. This may be appropriate for some consumers, but many will be missing out on potentially higher returns available from investing. At the other end of the spectrum, some consumers are taking on too much risk, with younger people twice as likely to have invested in HRIs than adults overall (12% vs 6%).

Accessing the right support is crucial to enabling consumers to make investment decisions, with consumers who receive support more likely to invest. Nearly half (49%) of consumers who had not received support in the last year held all their investible assets in cash, compared to a quarter (25%) of those who had (RDR/FAMR).

Chart

Data table

Advice is not reaching all parts of the market. Only 8% of UK adults have received financial advice. Robo advice is failing to fill this gap, with only 1.3% of adults having used this in 2020. The majority (54%) have received no support in making investment decisions. Revenue from adviser charging continues to be dominated by ongoing advice services (76%), with only a quarter (26%) accounted by one-off advice. Transactional advice is an important service for consumers investing smaller amounts of money.

Where consumers do receive advice, we continue to have concerns about the suitability of some of that advice. Latest figures show that 17% of DB-DC transfer advice was unsuitable and a further 28% had significant information gaps.

Few consumers have considered the benefits of advice. With nearly 70% (67%) of consumers believing they can make investment decisions themselves and a further 22% had simply not thought about it.

Chart

Data table

3.2. Our action on these issues

We think more consumers could benefit from investing and we want to remove regulatory barriers that prevent access and improve support. Over the years we, and other regulators, have looked to increase consumers’ ability to engage with the mainstream market and improve access to support.

Table 3: Summary of initiatives to improve the mass market

| Date | Initiative |

|---|---|

| April 2001 | Stakeholder products are introduced |

| 2005 | Basic Advice regime aims to enable firms to provide simpler and lower-cost advice on stakeholder products using pre-scripted questions (2005) but fails to get traction |

| April 2005 | Stakeholder products replace CAT standards |

| April 2011 | Money Advice Service launched |

| October 2012 - February 2018 | Auto-enrolment into workplace pensions mandated |

| 31 December 2012 onwards | Retail Distribution Review (RDR) bans commission and raises adviser professional standards |

| March 2015 | Retirement Income Market Study triggers improvements to pension and annuity information given to consumers as they approach retirement |

| April 2015 onwards | Pension freedoms introduced |

| March 2016 | Financial Advice Market Review (FAMR) highlights the lack of mass-market advice services |

| April 2016 | FCA Advice Unit set-up to help firms developing automated advice models (announced in 2016 Business Plan) |

| October 2016 | Investment and Corporate Banking Market Study leads to targeted measures to ensure competition operates effectively across lending and corporate broking services to primary market services |

| April 2017 | We establish the Financial Lives survey, our flagship nationally representative survey of UK consumers |

| June 2017 | Asset Management Market Study proposes measures to drive competitive pressure on asset managers |

| September 2017 | We issue new guidance on streamlined advice aiming to give firms confidence to provide streamlined services for simple consumer needs |

| January 2018 | PRIIPs Regulation comes into force, requiring firms to give consumers a standardised pre-contractual Key Information Document |

| June 2018 | Retirement Outcomes Review (June 2018) leads to the introduction, in February 2021, of ‘investment pathways’ for consumers preparing to enter drawdown or buy an annuity |

| March 2019 | Investment Platforms Market Study explores how investment platforms compete and prompts changes to make it easier for consumers to move platforms |

| December 2019 | We publish our decision to make a market investigation reference (MIR) to the Competition and Markets Authority (CMA) regarding investment consultancy services and fiduciary management services (September 2017). In December 2018, the CMA published its final report, leading to an order designed to improve the information given to and incentives facing pension trustees in choosing fiduciary management services (from December 2019) |

| September 2019 | Call for Input: Consumer Investments looks across the market and considers whether there are systemic issues that need to be fixed |

| December 2020 | RDR and FAMR Review highlights the potential for more tailored guidance and simpler advice services to help attract more consumers towards support in purchasing investments |

| January 2021 | Our first Consumer Investments Data Review reports on steps to protect consumers from investment harm by stopping and disrupting potentially harmful firms and activities |

| March 2021 | Britainthinks research for the FCA published: ‘Understanding self-directed investors’ explores consumers' complex and highly personalised investment journeys |

3.3. Short term strategy actions

We will continue our work on improving mass market consumer outcomes, starting with:

- Consumer Duty - We want to see a higher level of consumer protection in retail financial markets. We have consulted on a Consumer Duty that would set clearer and higher expectations for firms’ standards of care towards consumers. It would require firms to ask themselves what outcomes consumers should expect from their products and services, act to enable these outcomes and assess the effectiveness of their actions.

- Firm support - We have been working with individual firms to help them use the flexibility offered by the existing regulatory framework. This work will continue as we develop our broader approach to the mass market.

- Consumer journey - Our evidence shows that consumers fail to make decisions that optimise their pension saving. They may remain in poor-performing products - often originally chosen by their employer - and can be susceptible to scams. The Pensions Consumer Journey Call for Input closed for responses at the end of July 2021 and will help us understand how we can target future regulatory interventions at key points in the consumer journey to improve pension outcomes.

- Stronger nudges to pensions guidance - Pension providers are required to signpost consumers to Pension Wise guidance, a free and impartial guidance service for defined contribution pension consumers, at various stages of the consumer journey. We have consulted on proposed rules to give consumers a final opportunity to take Pension Wise guidance at the point they wish to access or transfer their pension savings.

- Vulnerability guidance - We published our final guidance for firms on the fair treatment of vulnerable customers in February 2021. We are working with firms to drive improvements in the way they treat vulnerable consumers, so that they experience outcomes as good as other consumers.

- Our new approach to consumer engagement - As well as delivering our new investment harms campaign, we will explore how best we and regulatory partners can engage and empower consumers directly. This includes helping people understand which protections apply to financial products.

3.4. Longer term strategy actions

We will take steps to improve the supply side of the market by making it easier for firms to give consumers the support they need and by ensuring firms prioritise good consumer outcomes in the design, communication and pricing of products and services.

Giving consumers the confidence to invest

We want more consumers to invest their money, when that is the right option for their circumstances. Many consumers find investments complex to navigate and we want firms to support them through this journey. So, we are exploring how we can make regulatory changes to make it easier for firms to provide more help to consumers who want to invest in relatively straightforward products. This will be restricted to the more straightforward ISA wrappers that do not contain high risk investments, and which are well diversified (such as tracker products).

We want to make changes so that firms are subject to proportionate requirements when they support new consumers to invest in products that suit their simple investment goals. We are collecting information from firms to help assess the commercial viability of our proposals, as well as analysing consumer research to identify how the proposed regime can successfully engage consumers. We plan to consult on our proposals early in 2022, so that they can be implemented at the start of 2023.

We will then consider how to allow firms to do more to support wider investment customers (such as existing investors) to make effective future investment decisions.

While we are not proposing kite-marking Financial Ombudsman Service and FSCS protections, the combination of this regime and our changes to the financial promotion regime set out in our chapter on higher risk investments should help further segment the high-risk market.

Improving outcomes for investors

Through the Consumer Duty we make it clear that we want firms to prioritise good consumer outcomes as an objective of their business priorities. How we supervise and enforce the Consumer Duty will the key to its success. We will provide further details of how we will work with firms in a second consultation that we expect to publish by the end of 2021, with new rules to be published by the end of July 2022. One of the outcomes we are seeking through the Duty is that products and services are specifically designed to meet the needs of consumers and are sold to those whose needs they meet (e.g. higher-risk investments products are not sold to consumers without sufficient capacity for loss).

4. Higher risk investments

4.1. What’s driving consumer harm

Higher risk investments have a place in a well-functioning consumer investment market. However, we are concerned that some investors access higher-risk investments which do not reflect their risk tolerance and are very unlikely to be suitable for them. Coronavirus (Covid-19) has accelerated some of these trends, with 6% of investors investing for the first time or increasing their holdings of high-risk investments during the pandemic (FLS).

Many consumers struggle with the complexity of investment decisions and may not fully understand the level of risk they are taking. 57% of adults indicate low financial capability or find it hard to find suitable financial products or services (FLS 2020). There is a lack of awareness of the risks of investing, with almost half (45%) of new self-directed investors unaware that ‘losing some money’ is a risk of investing (understanding self-directed Investors - Britain Thinks).

Consumers often can’t tell the difference between different types of investments and tend to focus on the promised returns. For example, FCA research found that consumers only start to recognise that a financial promotion for an investment product is probably ‘too good to be true’ when the promised rate of return is around 30% or more. The current rate of return on a cash ISA is around 1% per annum and consumers should be wary of returns offering significantly more than this.

Investment decisions are highly influenced by emotional and social drivers such as gut instinct, irrational exuberance, sunk-cost bias and perception of other people’s investment success. Four in ten new self-directed investors (38%) are being driven solely by these types of motivating factors (Britain Thinks).

Graph 3: Those investing in high-risk tend to have the highest confidence and self-perceived knowledge in investing

Chart

Data table

Chart

Data table

Advancements in technology have increased accessibility of retail investments, with trading apps growing rapidly. 1.15m new accounts were opened by 4 trading app firms in the first 4 months of 2021, almost double the amount opened with all other retail investment services combined (632,000). 50% of these were opened in January, driven by the surge in investments in GameStop and other meme stocks. Many consumers appreciate the ease of investing that these new channels offer, however this lack of friction makes it easier for consumers to make bad decisions and bypass existing support mechanisms.

Chart

Data table

Investors are being targeted by online adverts through social media promoting high risk products. With newer investors more likely to rely on social media to identify new investment opportunities (Britain Thinks).

Macroeconomic factors have also increased the demand for retail investing. For instance, low interest rates have driven a search for higher returns and the Pensions Freedom Act allowed consumers to access large sums of money to invest. Increased savings have also driven demand for retail investing. Since March 2020, the Bank of England estimates households have accumulated a large excess stock of savings of £125 billion.

4.2. Our action on these issues

Reducing harm from high-risk investments is an FCA priority and we use our full range of tools to protect consumers.

- Marketing restrictions: In January 2021 we extended and made permanent a ban on the mass marketing of speculative illiquid securities. During 2019 and 2020 we banned the sale, marketing and distribution of crypto-derivatives and binary options. In 2019 we also placed restrictions on the sale, marketing and distribution of Contracts for Difference.

- Preventing firms and individuals entering the gateway: We seek to prevent harm by ensuring that all firms and individuals meet our standards. We stopped 26 new firms from entering the market between 1 April 2020 and 31 March 2021, where the potential for consumer harm was identified (this figure has been updated following review).

- Regulatory oversight of the market: We supervise firms, and individuals controlling firms, by monitoring the way they conduct business; including 6,568 consumer investment firms. In 2020/21 over 1000 supervisory cases were opened involving higher risk investments or potential investment scams (this figure has been updated following review).

Chart

Data table

- Acting against firms and individuals who cause consumer harm: We decide whether to take enforcement action based on whether we believe there has been serious misconduct. Over 2020/21 we oversaw 5 public outcomes from enforcement actions against regulated firms and individuals and 11 against unauthorised firms and individuals related to high-risk investments or scams.

- Providing direct consumer support through our Consumer Helpline: In 2020/21, we received an average of more than 9,000 enquiries from consumers a month, with 10.9% relating to investment products and 5.1% related to pensions or retirement products.

Chart

Data table

4.3. Short term strategy actions

- Use of data and technology to spot harm faster - Our data strategy outlines how we are harnessing the power of data and advanced analytics to transform how we regulate. One of its key components is the enhanced use of data and technology to identify, predict and prioritise risks across populations of firms, sectors or products. A range of initiatives have been implemented, or are being developed, to enable us to spot harm sooner. These include:

- Dashboards which combine relevant data sets on a given firm, sector or issue. This makes it easier to spot new trends or areas for investigation.

- Automated, rules-based alerts which prompt regulatory action when one or more ‘red flags’ are triggered at an individual firm or sector level.

- Tools which use advanced analytics to increase our understanding of the potential harm at a firm or sector level.

- Investment Harm campaign - We are launching a campaign to help consumers make better-informed investment decisions. This new campaign will particularly target consumers investing in higher risk investments. Our campaign objectives are to provide information for consumers to identify investments that are suitable for their needs and risk tolerance. We plan to use a range of channels to reach our audience including, partnerships with influencers, social media, online videos, paid ads on google and more.

- Tackling out-of-date permissions - Incorrect or out-of-date permissions increase the risk of harm to consumers as they can mislead consumers about the level of protection offered or give credibility to unregulated activities, the so-called halo effect. We are undertaking a ‘use it or lose it’ approach to firms’ permissions to help reduce risk to consumers. Where we consider a firm is no longer carrying on regulated activities, we will consider cancelling a firm’s permission and expect to use the power introduced by the Financial Services Act 2021 to expedite this process. We are working to embed this approach and will publish an update on the number of firms who have given up or varied their permissions later in the year.

- Marketing restrictions - We have limited powers over many issuers of high-risk investments because they are often not carrying on regulated activities when they issue an investment product. This means that we cannot generally impose requirements on the issuers of high-risk investments themselves as these issuers are often not subject to our rules. However, we can make financial promotions rules applying to firms which approve promotions for such investments and which may regulate how, and to whom, those investments may be marketed. We will increase our horizon scanning of emerging harms and be more pro-active in restricting the marketing of high-risk investments where we see harm.

- Continue to strengthen our supervisory capabilities - We are using a web crawling and scraping tool to increase our understanding of how products and services are marketed to consumers online. It allows us to automatically search publicly available internet sources (including paid adverts), then download and analyse the resulting web pages. We have applied this to identify high risk financial promotions (eg those that promise very high returns or have a suspicious business model) and scams, allowing us to intervene earlier to prevent consumer harm.

4.4. Longer term strategy actions

Strengthening the financial promotion regime

On 29 April, we published a Discussion Paper on strengthening financial promotions rules for high-risk investments. The paper builds on our recent permanent ban on the mass-marketing of speculative illiquid securities and the Treasury's consultation on creating a new regulatory gateway through which authorised firms would need to pass to be able to approve the financial promotions of unauthorised firms. We are looking to strengthen our rules in 3 areas; our classification of high-risk investments, further segmenting the high-risk market and strengthening the requirements on firms when they approve financial promotions. We will use the feedback from this Discussion Paper, alongside further analysis and behavioural testing, and intend to consult on new rules later in the year.

Organise more effectively

We are transforming to ensure we can make fast and effective decisions and can prioritise the right outcomes for consumers, markets and firms. These objectives require us to reform our approach to how we gather and use intelligence and information. These reforms are vital so we can sustainably oversee over 50,000 firms under our remit and effectively make the difficult choices about where to allocate resources this entails.

5. Scams

5.1. What’s driving consumer harm

Investment scam activity is growing significantly with fraud volumes, fraud losses and enquiries to our Consumer Support rising.

Table 4: Year-on-year changes in key scam indicators

| Apr 2019 – Mar 2020 | Apr 2020 – Mar 2021 | YoY % change | |

|---|---|---|---|

| Supervision Hub – Investments & pensions calls reporting possible scams | 9,272 | 16,853 | ↑ 82% |

| Enforcement – Reports of unauthorised business | 19,574 | 30,122 | ↑ 54% |

| Action Fraud – Investment fraud reported volumes | 14,024 | 23,378 | ↑ 67% |

| UK Finance – Investment Scams losses | £95.4m [in 2019] | £135.1m [in 2020] | ↑ 42% |

Several factors contribute to creating opportunities for scammers. Social media and digital distribution provide channels through which scammers can target consumers, with the number of consumers calling our Consumer Helpline about scams perpetuated through social media more than doubling in 2020. Consumer desire for high returns and a lack of financial knowledge can contribute to consumers falling victim to scams, with 57% of adults indicating low financial capability (FLS).

Chart

Data table

Psychological and behavioural factors can also make consumers vulnerable to scams. Self-investors tend to have a high degree of confidence they can spot scams, but rely on an investment opportunity ‘not feeling right’ or looking unprofessional (Britain Thinks). This creates vulnerabilities to scammers which look legitimate and scammers often exploit this by spoofing (changing their caller ID to legitimate sources such as HMRC or the FCA). Enquiries to our Consumer Helpline about FCA impersonation scams were up over 150% in 2020/21.

Chart

Data table

5.2. Our action on these issues

We already tackle many different types of fraud. For example, through our targeted ScamSmart campaigns, our information sharing and cooperation with external partners, our Supervision and Enforcement work on financial promotions and our work to disrupt unauthorised businesses who seek to defraud consumers.

- Acting against unauthorised business: We take enforcement action against firms and individuals that are not authorised or exempt under FSMA but who carry on regulated activities in breach of the legislation. In the financial year 2020/21 we received over 30,000 reports about potential unauthorised business activity and issued 1,317 consumer alerts. We pursued 50 enforcement investigations against unauthorised business in 2020/21, with approximately £21.7m being awarded under restitution orders for unauthorised investment business and nearly £7m being frozen on behalf of investors pending court judgments.

- Supporting consumers who suspect scam activity: Consumers reported 30,000 potential scams to us, with investment scams accounting for 58% of these enquiries. This is 82% higher than in the previous 12 months.

- Supporting consumers to spot scams: Our ScamSmart campaign aims to empower consumers with the knowledge and tools to help prevent them falling victim to scams. The campaign focuses on raising consumer awareness of the key warning signs associated with a scam and driving use of our Warning List tool. 125,000 people visited our ScamSmart website in 2020/21 and 24,000 searched our Warning List for a firm. We will continue to promote the campaign and consider how we can better make use of rules of thumb to enable consumers to spot potential scams.

Chart

Data table

5.3. Short term strategy actions

- The role of technology platforms - Online platforms, such as search engines and social media platforms, play an increasingly significant role in disseminating promotions of financial products and services. This includes adverts which expose consumers to significant risk of harm such as promotions for high risk investments which are unsuitable for most investors, adverts which make false or misleading claims and scams which may or may not fall within our jurisdiction. We note that since the end of the Brexit Implementation Period earlier this year, an exemption to the financial promotion restriction available to online platforms has fallen away. As a result of this change, we are looking at the operations of the major online platforms to determine whether they are now subject to the restriction and, if so, whether they are compliant. Where they are not, we will take action to ensure consumers are protected.

- Delivering the FCA’s counter-fraud approach - We are working to identify what further actions we can take to build on our existing work and contribute to a more effective collective effort to fight fraud in the UK, particularly through prevention and disruption. This will include conducting proactive surveillance, working collaboratively with other agencies to disrupt the work of fraudsters and exiting fraudsters who are FCA-supervised.

6. Redress

6.1. What’s driving consumer harm

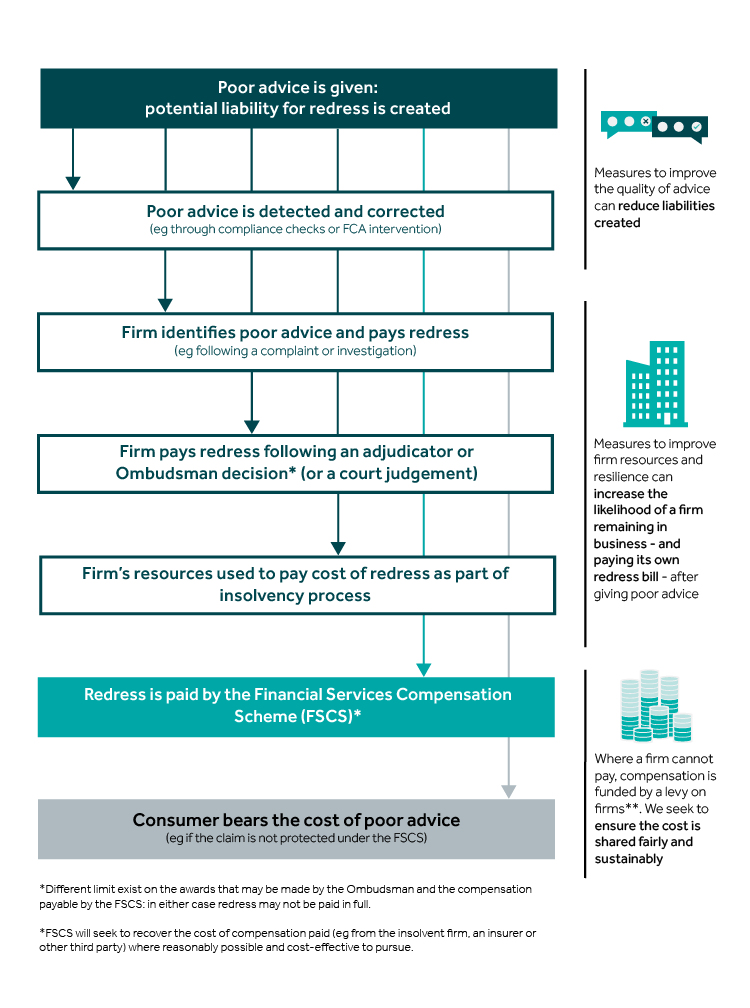

Poor advice given generates a liability. A consumer who becomes aware of this during the firm’s lifetime can seek redress via a firm’s complaints mechanism or the Financial Ombudsman Service. However, consumers will not always become aware of the problem during the firm’s lifetime, or redress required by the Financial Ombudsman Service to address misconduct may make a firm insolvent. In these cases, consumers may be able to make a claim to the FSCS and any compensation is paid for by the firms remaining in the market. The FSCS will then seek to recover some of the costs from the firm that generated the liability.

Infographic 3: Looking at the different ways that poor advice is paid for

View accessible version of infographic (PDF)

Adviser firms pay redress from their own financial resources and via PII. However, capital set aside is often insufficient to pay for redress, with the minimum capital requirement for most adviser firms set at only £20,000. This compares to £66.7m of redress paid in response to investment complaints (£1,172 per upheld complaint) in 2020. Putting right even a single complaint for poor advice can be expensive, which is reflected in the limit on a single Financial Ombudsman Service award being set at £350,000.

Pensions and investments complaints have risen by 16%, as overall complaints (non-PPI) are down 4%, indicating the potential for future redress liabilities to remain high.

Chart

Data table

The PII market has hardened, both in terms of reduced access and increased prices. The number of insurers active in this market has fallen from around 15 to 5 in the last 5 years and we understand that PII costs for firms that have previously advised on Defined Benefit pension transfers have increased from around 1-1.5% to 3-6% of firm income.

These factors will have contributed to firms finding themselves unable to meet their liabilities, which then pass to the FSCS. The FSCS estimates that their compensation levy costs for the 2021/22 financial year will be £833m, up 19% on 2020/21. The consumer investments market is responsible for most of these liabilities. With claims arising from the Life Distribution and Investment Intermediation class (LDII) and Investment Provision accounting for around 72% of this (£618m). These liabilities have led to both LDII and Investment Provision classes breaching their funding limit for the last 2 years. As a result, firms from across retail financial services are having to contribute to costs being generated by firm failures originating in other funding classes.

Chart

Data table

Annual pensions and investments FSCS claims have grown from £130m to £453m.

6.2. Our action on these issues

Improving the quality of advice given or the ability of the firm to cover the cost when it does make a mistake can, over time, reduce the burden of FSCS costs. Our day-to-day work already focuses on both of these areas.

- Addressing poor advice: This remains key in our ongoing supervision, multi-firm and past business reviews, as well as enforcement action. This is complemented by policy work, including work on DB-DC transfers to increase and drive a clear understanding of standards expected. Firms and individuals who seek to avoid the liabilities and ‘phoenix’ back into the market are tackled at our authorisations gateway. Relatively few firms give rise to extreme redress liabilities far in excess of their size, with a very small minority giving rise to over £10m of compensation each. We want to strengthen firms’ resilience where they make mistakes, but we also need to continue to clamp down on bad actors – and for industry to work with us to strengthen standards and address poor practice in all its forms.

- Strengthening capital standards: The new Investment Firms Prudential Regime will change how the capital requirements are calculated for adviser firms that would previously have been subject to the Markets in Financial Instruments Directive (MiFID).

- Reviewing FSCS funding: We also reviewed FSCS funding from 2016 to 2018, resulting in changes intended to reduce the volatility of FSCS levies and deliver a robust funding model. The changes included a requirement for product providers to contribute to insurance and investment intermediation funding, lessening the impact on intermediaries.

6.3. Short term strategy actions

It takes time to drive improvements in firms’ systems and controls, resources and resilience that could lead to a reduction in poor advice given and the need for redress. But there are some steps we can take in the meantime.

Our work to improve the quality of advice

- Address misuse of the Appointed Representatives (ARs) regime - Principal firms who use ARs are, as a whole, responsible for more complaints and redress (weighted by activity) than non-principals. This has the potential to translate into significant redress liabilities over time. As part of our wider Appointed Representatives work, which we announced in our recent Business Plan, we are increasing our supervision activity to reduce the risk posed by ARs. As well as activity focused on high-risk principals we will be increasing our scrutiny of firms when they appoint ARs.

Table 5: complaints and redress paid principal vs non-principal firms

| Retail Investments Intermediaries | Non principal firms | Principal firms and their ARs |

|---|---|---|

| Revenue from RMAR (2018 – 2019 H1) | £2.36bn | £2.81bn |

| Mean firm complaints per £m of revenue | 1.74 | 3.73 |

| Mean Financial Ombudsman Service complaints per £m of revenue | 1.06 | 1.21 |

| FSCS claims (2018 – 2019 H1) | £392.6m | £641.0m |

- Continue to strengthen our ability to prevent poor advice at the gateway - We have improved our insights into how companies and individuals are related, helping us to quickly identify where dishonest firms and individuals may be involved and spot suspicious activity such as ‘phoenixing’. This is made possible by the development of a new network analytics tool that links data from a variety of sources, including external datasets, and plots interrelationships as a visual network map. This will enhance our capacity to stop potentially harmful firms from entering at the gateway and provide insight for Enforcement investigations.

Our work to improve firm resources and resilience

- Investigate the potential impact of changes to adviser capital - alongside other measures to reduce the redress bill. While it’s unlikely that we could ever set capital requirements at a level that would ensure firms could pay for redress, higher capital requirements could be used, for example, to prompt firms entering the market to think carefully about giving advice in high-risk areas. We propose to explore the impact of different changes to our capital requirements for non-MiFID adviser firms – taking into account the potential impact on the cost of and access to advice for consumers.

- Create conditions for firms to demonstrate good advice - We are interested in the ways that firms demonstrate that they have given good advice, so they can secure PII that is appropriately priced. We are exploring whether there are ways to support firms better in demonstrating the quality of the advice they have given (eg through use of third-party audit).

- Responding to changes in the PII market - We are continuing to monitor developments in the market for PII and will communicate with firms about our expectations.

6.4. Longer term strategy actions

In the longer term, we may have greater ability to drive improvements in the resources and resilience of firms that give investment advice, as well as the quality of their oversight and control of the advice they give. As we make changes, we aim to see the burden of compensation costs falling in the years ahead.

Our work to improve the quality of advice

- Address misuse of the Appointed Representatives (ARs) regime - We propose to consult on changes to our rules, to clarify our expectations of principals and thereby ensure that we can more effectively challenge Principals about their ability to oversee the activities of ARs, before harm occurs. We are also engaging with the Treasury about the potential for legislative change to strengthen the regime for Principals and ARs.

Our work to improve firm resources and resilience

- Reviewing our adviser capital requirements (for non-MiFID firms) - We will consider consulting on changes to the specific capital requirements for non-MiFID adviser firms, taking account of the need to introduce such changes on an appropriate timescale. Increasing capital requirements for higher risk business has the potential to improve firm resilience and ability to pay redress over time. We will also consider changes to our requirements on holding PII, if appropriate.

Looking at what happens when a firm cannot pay

- Reviewing the compensation framework - We will review the compensation framework to ensure that it remains proportionate and appropriate particularly where firms fail leaving behind compensation liabilities for FSCS to address. We plan to publish a discussion paper later this year.

- Examining ongoing levels of compensation and consumer protection - Through our consumer investment strategy as a whole, we are exploring ways to support and guide consumers towards mainstream, well-diversified products, when they enter the investment market – and away from high risk investments where these are inappropriate for them. As we make progress, we will examine the case for rethinking the extent of FSCS protection available for the minority of consumers who make an active choice to purchase particularly high-risk investments.

7. How the strategy will be delivered

7.1. Strategy Road map

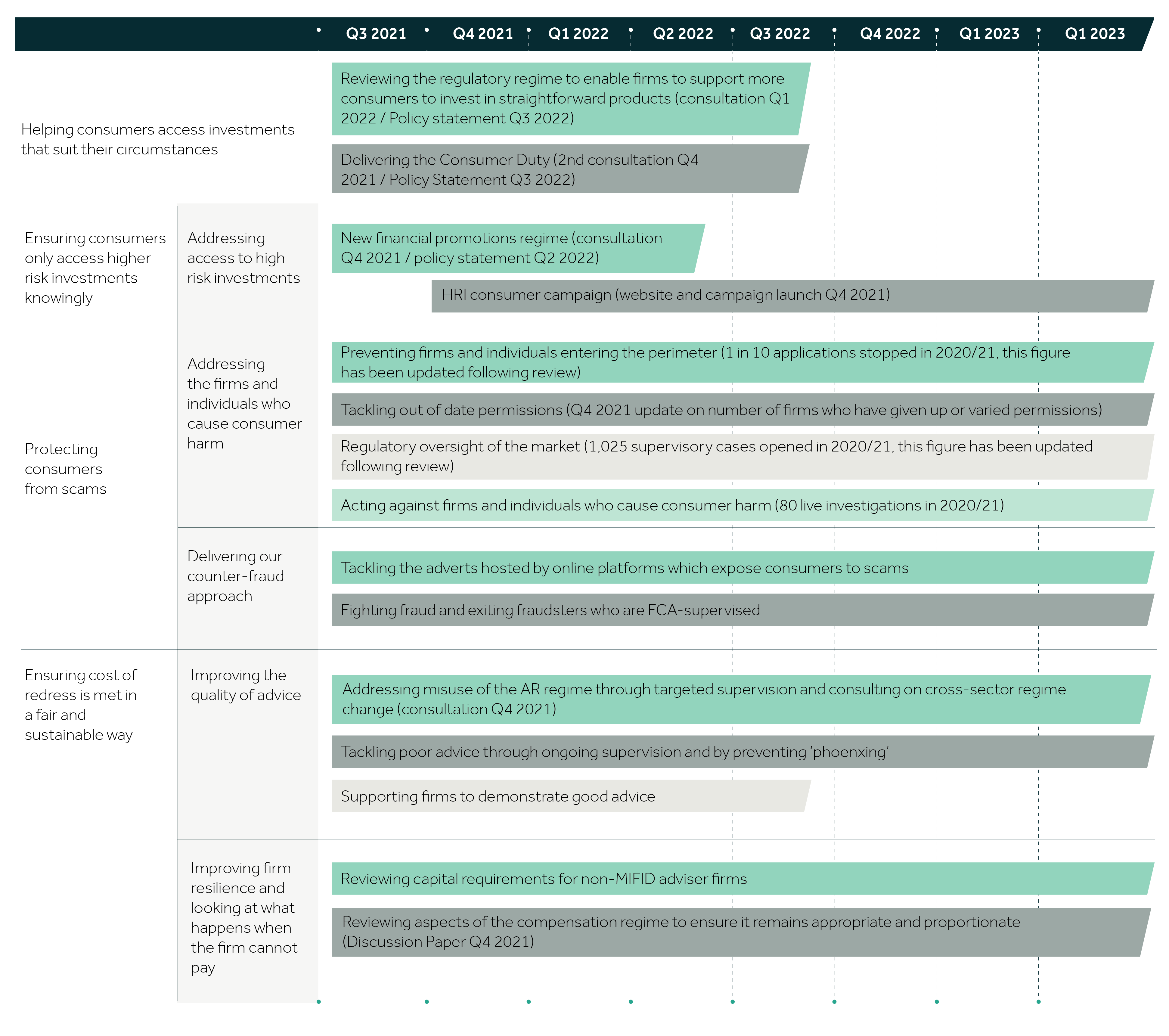

Our Business Plan 2020/21 announced that the consumer investments market would be a business priority for the next 3 years. Our strategy will be delivered by April 2023. The table below outlines the key impact points.

Infographic 4: Road map

7.2. Working with our regulatory partners

Tackling harm in the consumer investment market requires a collective effort. We continue to work closely with our regulatory partners including the Financial Ombudsman Service, FSCS and MAPs as well as other agencies such as the Home Office, the NECC and law enforcement agencies. Alongside this existing engagement, we have created a ‘consumer investment coordination group’ involving FCA, FSCS, the Financial Ombudsman Service and the Money and Pension Service (MaPS). This will identify areas of joint working to tackle harms in the consumer investments market and ensure efficient coordination on key workstreams.

This market is constantly evolving, and we welcome continued feedback on our approach. We will also gather information on sharp practices in this market so we can better target where we intervene.

7.3. Measuring outcomes

Our strategy is focusing on 4 key outcomes. By defining these outcomes, measuring them and acting on the results with an enhanced data capacity, we are able to target our interventions more effectively. Being transparent about the outcomes we seek and publishing metrics so that people can judge whether we are achieving them also provides better accountability and ensures that both we and the firms we regulate are called to action when things are not going right. No single metric can tell us whether harm is decreasing in this market, so we will be monitoring a range of other data on an ongoing basis to track harm in this market.

| Mainstream investments | 20% reduction in the number of consumers with higher risk tolerance holding over £10,000 in cash by 2025 (FLS) Baseline: 8.6 million consumers hold over £10k investable assets in cash (2020) Targeted levels: 6.9 million by 2025 |

|---|---|

| High risk investments | 50% reduction in the number of consumers investing in HRIs who indicate a low risk tolerance or demonstrate characteristics of vulnerability by 2025 (FLS) Baseline: 6% of adults were invested (3.15 million) in HRIs during the pandemic (2020) Targeted levels: 3% (1.57 million) by 2025 |

| Scams and fraud | Seek to reduce the amount of money consumers lose to investment scams, through reductions in investment scams perpetrated or facilitated by regulated firms (Action Fraud).* Baseline: £569m lost to investment fraud in 2020/21 Targeted levels: Reduction on the £569m lost to investment fraud in 2025 |

| Consumer redress | Act to stabilise the LDII and Investment Provision funding classes by 2025, and target a year on year reduction in these classes from 2025 to 2030 Baseline: FSCS Outlook May 2021, forecast for 2021/22

Targeted levels: 2025-£618m, 2025-2030 year-on-year reduction |

* We will review the metrics we use for our baseline when there is greater clarity on the future of the UK’s fraud reporting.

7.4. External reporting

We are rightly accountable for our work to protect consumers. We will continue to publish our Consumer Investments data review which provides transparency about our activities. Our second review covering April 2020 to March 2021 is published alongside this strategy. This report will evolve over time to enable us to report on our progress in achieving our strategy outcomes.

Finally, we need to be open about our long-term vision for financial services, including the consumer investments market. We’ve set out the focus of our role and the changes we’re making to meet current and future challenges in our Business Plan 2021/22. In early 2022, we will publish our wholesale and retail strategies to set out our ambitions for these markets.