Key findings from the FCA’s Financial Lives 2020 survey and October 2020 Covid-19 panel survey.

Introduction

Financial Lives, our flagship survey of UK consumers, provides a wealth of information about consumers’ attitudes towards managing their money, the financial products they have and their experiences of engaging with financial services firms. It is unique in the combination of its design, its breadth (over 1,300 questions covering all the retail sectors that we regulate) and its size (over 16,000 respondents in the latest wave). As a tracking survey, it provides evidence of how things are improving, worsening or staying the same, from the point of view of the consumer.

As a consumer-focused and data-led regulator, it is vital that we have the insights to understand the realities of consumers’ changing financial lives. The Financial Lives nationally representative data help us to deliver our consumer protection and competition objectives through identifying harm and improving consumer outcomes. The data also provide valuable insights for the financial services industry, the Government, policy-makers, consumer bodies and academics.

Our second Financial Lives survey ended in February 2020 before the pandemic. It therefore gives us an understanding of consumers’ financial positions before the coronavirus (Covid-19) pandemic. This tells us much about their likely ability in February 2020 to deal with financial shocks. It also means that the survey acts as a baseline against which to understand changes in people’s financial situations during and after the pandemic.

To test how the pandemic had already affected UK consumers, we ran a survey – our Covid-19 panel survey – in October 2020 with over 22,000 respondents. We will use future research and analysis – including our next Financial Lives survey – to understand the changing shape of consumers’ financial lives after the pandemic.

This executive summary is in two parts. In the first part, we look at how the market has evolved since our first Financial Lives survey in 2017 to early 2020. We look in particular at how many UK adults had low financial resilience or were otherwise not well positioned to deal with the financial impacts of the pandemic. In the second part, we focus on the impacts of Covid-19 on UK adults’ financial lives, drawing largely on our bespoke Covid-19 focused survey from October 2020.

See Chapter 1 (Introduction to the Financial Lives survey) for more information on the research used in this report.

Consumer trends from 2017 to early 2020

Consumers with characteristics of vulnerability

All consumers are at risk of becoming vulnerable (and hence at greater risk of harm), particularly if they display characteristics of vulnerability to do with poor health, a life event, low resilience or low capability.

In 2017, 51% of UK adults (26.0m) showed one or more characteristics of vulnerability. By February 2020 this proportion had fallen to 46% (24.0m). This was largely due to fewer being digitally excluded (14% in 2017 vs. 9% in 2020) and fewer having low financial resilience (23% in 2017 vs. 20% in 2020).

Older people aged 75+ saw the largest improvements in digital inclusion in this period (41% were digitally active in 2017, compared with 64% in 2020), and financial resilience improved broadly among 18-69 year olds.

But, looking at adults with characteristics of vulnerability in February 2020 indicates many people were already struggling to interact with financial services before the pandemic. Examples include:

- Adults with poor mental health or low mental capacity or cognitive difficulties: 42% of these people found dealing with customer services on the phone confusing or difficult; 34% were anxious when shopping around for financial products and services; 33% put off dealing with financial matters, such as ignoring warning letters, and 29% had fallen into debt because they had not wanted to deal with difficult financial situations.

- Adults with a physical disability: 33% of these people faced difficulties getting to a bank branch, while 30% found dealing with customer services on the phone confusing or difficult.

- Adults with a hearing or visual impairment: 40% of these people found dealing with customer services on the phone confusing or difficult; 38% faced difficulties getting to a bank branch, and 25% struggled to follow instructions which makes it hard for them to interact with financial services providers.

- Adults who had a relationship breakdown in the previous 12 months: 20% of these people had fallen into debt because they did not want to deal with difficult financial situations, while 20% struggled to manage their money.

- Adults with low capability about money and finances: 57% of these people felt nervous, overwhelmed or stressed speaking to financial services providers or found it hard to find suitable financial products or services; 37% struggled to assess financial products or found it difficult to shop around, while 16% had fallen into debt which might have been avoidable if they had understood their options better.

Low financial resilience

People are described as having low financial resilience if they are over-indebted or have little capacity to withstand financial shocks. For example, they could not withstand even a £50 reduction in their monthly income or losing their main source of household income for even a week.

Before Covid-19, 20% of adults (10.7m) had low financial resilience as Figure ES.1 shows.

Figure ES.1: Vulnerability, low financial resilience, over-indebtedness and being in financial difficulty (Feb 2020)

For source information, see Appendix B in the full report.

Of these adults with low financial resilience, 7.2 million (equating to 14% of UK adults) were over-indebted, and of these we define 3.8 million as being in financial difficulty (7% of UK adults) because they had missed paying bills or meeting credit commitments in three or more of the previous six months.

This was a slight improvement on the 2017 results, where 11.6 million (23%) had low financial resilience, 7.5 million (15%) were over-indebted and 4.1 million (8%) were in financial difficulty. Financial resilience improved in this three-year period more so for men than women (18% of men had low resilience in 2020, down from 21% in 2017, compared with 24% and 23% for women, respectively). The improvement spans all ages groups from 18 to 69.

In February 2020, certain demographic groups were far more likely than others to have low financial resilience, and therefore be at greater risk of harm. Those least able to cope with a financial shock included: unemployed adults (47%), renters (47%), adults with a household income of less than £15,000 (43%) and Black adults (34%).

Warning signs

People with low financial resilience were in the worst financial position before Covid-19. Many others, however, only had limited financial resilience in early 2020.

Having money set aside in an accessible savings buffer, to pay for an unexpected expense or to draw on if you lose your job, is a sensible plan. While the amount that should be set aside might vary according to each individual’s circumstances, financial experts generally recommend a figure of at least three months of expenses. Yet, in February 2020, 39% of adults (20.3m) said they could only continue to cover their living expenses for less than three months, if they lost their main source of household income.

People who use credit may be able to cope under ‘normal’ circumstances, and some will have no problems, such as those who pay off their credit or store cards every month. But a sustained income shock may push some into difficulties. This may be particularly true for those who are borrowing using high-cost credit or have levels of borrowing that are unsustainable. For example, in February 2020:

- One in ten (10% or 5.1m) were constantly or usually overdrawn. There was no significant change in these numbers between 2017 and early 2020. Many were using their overdraft facility to pay for essential living expenses, such as their rent or mortgage payments.

- One in twenty (5% or 2.8m) had persistent credit card debt because they were revolving a balance on a credit card and had paid more in interest, fees and charges over the previous 12 to 18 months than they had actually paid off on their card(s).

- One in ten (11% or 5.6m) held one or more high‑cost loans, unchanged from 2017 (10%). It was very common for people to be using high-cost credit to cover day-to-day expenses.

- Less than 0.5% (0.2m) told us they had borrowed from an unlicensed moneylender or another informal lender in the previous 12 months, unchanged from 2017.

- A fifth (20%) of mortgage holders (3.5m) had outstanding mortgage debt at least four times their annual household income. This was a significant increase on the 14% of mortgage holders in 2017.

In total, 23.7 million adults (45%) were unable to cover their living expenses for three months or more or were borrowing in one of these ways in February 2020. This placed them at greater risk if they were to experience a persistent drop in income, for example due to furlough or losing their job.

Trust in financial services

A lack of trust and confidence can result in consumers not engaging with the financial services industry, or failing to address their own financial needs.

In February 2020, only 42% of adults had confidence in the UK financial services industry, up from 38% in 2017. And just 35% agreed that financial firms are honest and transparent, up from 31% in 2017. People with characteristics of vulnerability and the over-indebted were more likely than average to lack confidence in the industry.

Similarly, trust in the different retail financial sectors remains low across the board. In February 2020 banks came out top, but were trusted highly only by one in five adults (20%). Only 7% expressed high trust in insurance companies.

A more positive picture emerges when consumers rate their own provider. People generally have higher levels of trust in their own provider than they do in the sector in general.

Levels of product holding

There has been limited change in product holdings since 2017. The most significant increases are in pensions and e-money:

- Auto-enrolment has increased pension take-up: 70% of non-retirees in February 2020 had a pension in accumulation, up from 62% in 2017. Pension take-up has increased particularly among employees aged 25-54 (90% had a pension in accumulation in February 2020, up from 82% in 2017).

- E-money alternative account use has increased fourfold – from 1% in 2017 to 4% in 2020. Usage is particularly prevalent among men aged 18-34 where 9% held an e-money alternative account in February 2020, compared with just 3% in 2017.

Before Covid-19, 77% of adults (40.5m) had a savings account of any type, up from 72% in 2017. The most widely held products were savings accounts with a bank, building society or with NS&I, cash ISAs and premium bonds. A third (33%) of adults (17.3m) held any investment product, up from 29% in 2017. Older adults were far more likely to have savings and investments than younger adults. However, as we have already seen, few savers had any substantive savings in these accounts.

The use of credit was high in February 2020 and had been increasing. Use of FCA-regulated consumer credit increased from 46% of adults in 2017 to 51% in February 2020. Informal borrowing from friends and family had also been increasing, up from 7% of all adults in 2017 to 10% in 2020. For young adults aged 18-24, 19% borrowed from friends and family, up from 12% in 2017.

In contrast, there were positive signs that the levels of unsecured debt, although high, were on a downward trend. Excluding student loans, adults owed on average £2,960 in February 2020, down from £3,320 in April 2017. Average debt levels peaked for adults aged 35-44.

The proportion of people holding any insurance product has increased from 81% in 2017 to 88% in 2020. However, in early 2020 there remained a significant protection gap, as just over half (53%) did not hold any protection products at all. Encouragingly, this was a marked improvement on the 2017 figure, where 59% had no protection in place. In early 2020, the protection gap was most prevalent among those aged 18-24, unemployed, renting, single, with no educational qualifications, with low or no confidence in managing their money, Asian, Black, or with characteristics of vulnerability.

Digital access to essential banking services

Consumers are switching away from traditional channels to embrace digital solutions in banking:

- Branch use has declined significantly. In the 12 months to February 2020, 50% of adults with a day-to-day account carried out banking activities face to face in-branch, down from 63% in 2017. Despite this, usage remains high among older adults.

- Online banking has increased significantly in popularity among older age groups. In February 2020, 72% of adults aged 65-74 and 54% of adults aged 75+ banked online, compared with 60% and 27% in 2017, respectively.

- Younger adults have been moving away from online banking towards mobile banking. For example, in 2020, 60% of 18-24 year olds banked online, down from 84% in 2017, while 88% banked using a mobile app, up from 73% in 2017. Of note is the increased use of mobile banking apps in the older population: up from just 1% in 2017 to 14% in 2020 for those aged 75+, and up from 10% to 24% for those aged 65-74.

- 84% of adults have used an ATM to withdraw money or check their balance. Since 2017, there has been a decline in ATM usage among young adults aged 18-24 (77% in 2020, compared with 89% in 2017), but an increase in usage among those aged 75+ (67% and 54%, respectively).

Innovation and new technology are making digital payments easier than ever for consumers of all ages. In February 2020, 84% made a contactless payment in the previous 12 months, up from 63% in 2017.

New service providers are disrupting the traditional role banks play in the payments ecosystem. Nearly three in five (59%) used PayPal to pay for goods and services in the 12 months to February 2020, up from 47% in 2017.

The use of mobile wallets is also growing rapidly, doubling from 13% in 2017 to 27% in February 2020. Mobile wallets were more likely to be used by men (31%) and by those aged 25 to 34 (46%) or 18 to 24 (51%).

The market for Payment Initiation Services (PISs) is still in its infancy, but, in early 2020, one in ten (9%) adults had used these services. PISs were more likely to be used by women (10%), students (12%), those who are in financial difficulty (15%) and those aged 18 to 24 (16%).

Cash remains a vital payment method for many, including the most vulnerable in society. In February 2020, 5.4 million adults (10%) relied on cash to a very great or great extent in their day-to-day lives. Dependency on cash was highest among adults aged 85+, but it is not limited to this age group. In February 2020, 42% of those aged 85+ relied on cash. It is not possible to say how reliance on cash has changed over time, as the question was not asked in 2017.

The impacts and experience of Covid-19

Consumers with characteristics of vulnerability

Between March and October 2020, the number of adults with characteristics of vulnerability increased by 3.7 million to 27.7 million. A 15% increase on the February figure, this takes the overall proportion to 53% of all adults. This increase has been driven mostly by more people experiencing negative life events, particularly redundancy or reduced working hours (up 45%, from 20% of adults in February to 29% in October) and having low financial resilience (up 35%, from 20% of adults in February to 27% in October).

Those experiencing a negative life event in the preceding 12 months increased from 10.5 million (20%) in February to 15.3 million (29%) in October. In this period, ie from the end of February to October, over a quarter (27%) of all employees were furloughed for any length of time. This includes 4% who were put on paid leave, but not under the Coronavirus Job Retention Scheme. One in six (17%) employees reported that their employer had cut their hours, while less than one in ten (7%) had their hours increased or worked overtime. Seven in ten (71%) self-employed businesses experienced a reduction in business revenues between March and October. One in ten (9%) ceased trading altogether.

Covid-19 has had a disproportionate impact on those of working age. The largest proportional increases in vulnerability since February 2020 – by more than 40% –have been among younger adults aged 18-34 and the self-employed. In contrast, retirees have seen a small proportionate decrease in the numbers who have characteristics of vulnerability.

Our results are not showing a significant overall increase in the proportion of people saying they have a health condition or illness that reduces their ability a lot to carry out day-to-day activities (although this could have changed since October 2020, when the research was conducted). Covid-19 appears, however, to be having a significant impact on mental health, which can result in a range of difficulties when dealing with financial services. In October 2020, 18% told us they had a mental health condition or illness, up from 12% in February 2020. Over two-fifths (43%) of these were aged 18-34.

Our Covid-19 panel survey asks about emotional resilience. One in fourteen (7%) of all UK adults said they find it very difficult to recover from negative experiences. In total, 1% have low emotional resilience but no other characteristics of vulnerability. Including the emotionally vulnerable would increase the proportion of people with characteristics of vulnerability from 53% to 54% in October 2020.

Impact on finances and financial resilience

Chart

Data table

Base: All UK adults (Oct 2020:22,267), excluding ‘don’t know’ responses (3%)

Question: F16 (Rebased). Thinking about your financial situation overall, to what extent have you been impacted by the Covid-19 pandemic to date?

Note: This question uses a seven-point scale. Two codes have been condensed to ‘a lot worse’ and another two codes to ‘a lot better’.

Three in eight adults (38% or 20.0m) have seen their financial situation overall worsen because of Covid-19; 15% (7.7m) have seen it worsen a lot. Groups that have been particularly hard hit include: the self-employed, adults with a household income less than £15,000 per year, those aged 18-54, and BAME adults.

While these numbers are of course concerning, our results also show that almost half of adults (48% or 24.9m) have not been impacted financially by Covid-19, while one in seven (14% or 7.5m) have seen an improvement in their financial situation overall.

Comparatively, the retired population has been better insulated from the financial impacts of Covid-19. This is perhaps not surprising as key sources of income for this group – the State pension and defined benefit pensions - have not changed.

Female, 55-64

Male, 25-34

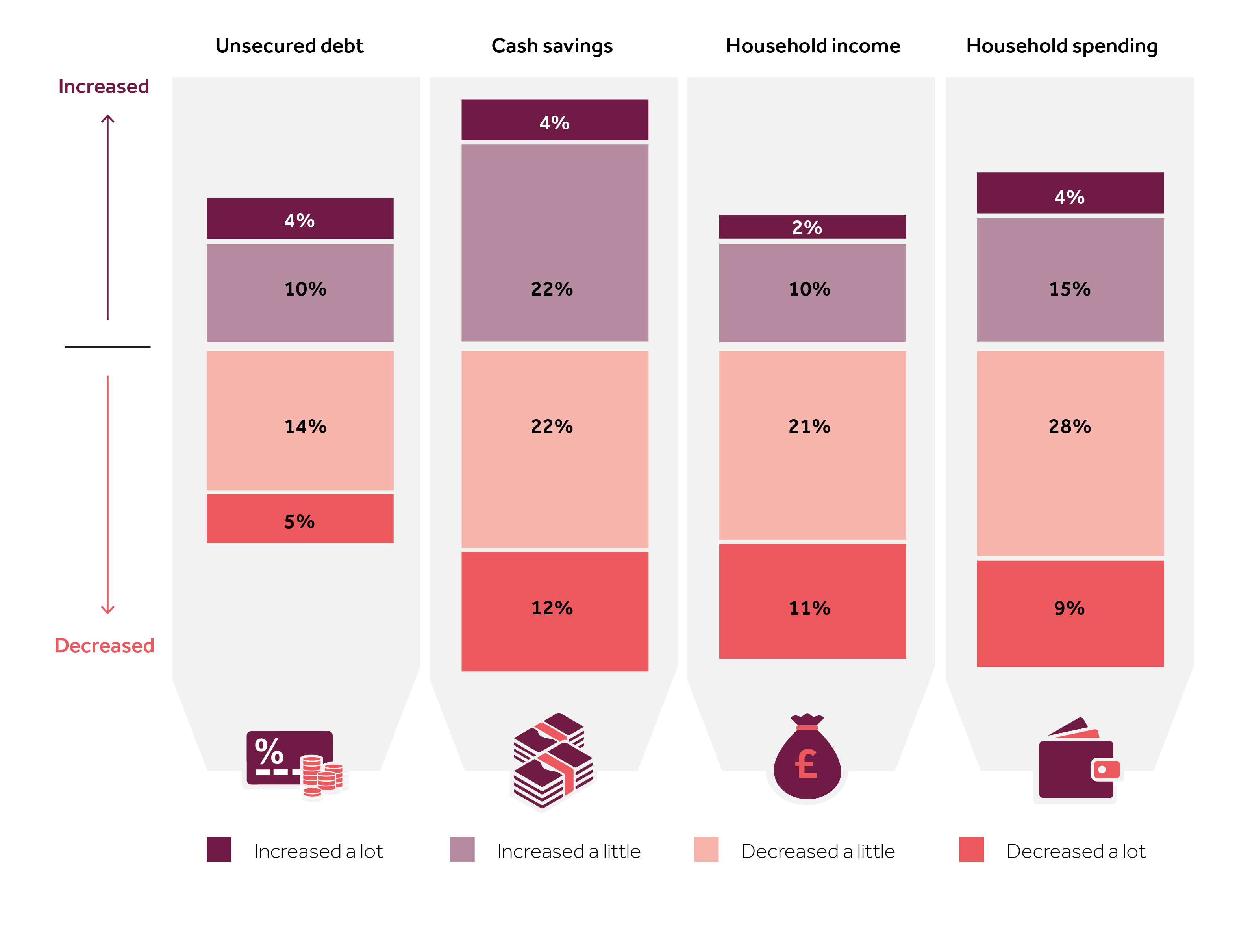

Given the severity of the lockdown restrictions, limitations on consumer activities, and the resulting impact on the UK’s labour market, it is perhaps not surprising to see that there have been both positive and negative financial impacts of Covid-19. These are summarised in Figure ES.3.

Figure ES.3: Adults who say their unsecured debt, cash savings, household income and household spending has increased or decreased since February (Oct 2020)

Source: Covid-19 panel survey, Oct 2020

Base: All UK adults (October 2020:22,267), excluding ‘don’t know’ responses (2%/ 1%/ 1%/ 1%)

Question: F1 (Rebased)/ F4 (Rebased)/ F7 (Rebased)/ F10 (Rebased). Comparing your … now and at the end of February. Overall, has your … increased, decreased or stayed the same?

Note: The base for ‘cash savings’ is those with any cash savings at the end of February

Positive impacts include 37% of adults reporting an overall decrease in their household spending, 12% experiencing an increase in household income, and 19% reducing their unsecured debt.

Male, 25-34

Between March and October 2020, the number of people with low financial resilience increased by 3.5 million from 10.7 million to 14.2 million. Those with low financial resilience now account for a quarter (27%) of adults.

This is not surprising given the large number of adults who, before Covid-19, had limited savings or had patterns of borrowing that placed them at greater risk if they experienced a persistent drop in income.

Looking at the groups which have been most affected since February 2020, the largest proportional increases in low financial resilience – by 40% or more – have been among those aged 18-54, and particularly younger adults aged 18-34. Adults in employment in February (employees and the self-employed) have been affected more than those who were then unemployed or retired.

We asked adults in October 2020 about their expectations for the next six months. This was before the announcement of the second England-wide lockdown that began in early November 2020 and the extension of the furlough scheme and payment deferrals. Some local lockdowns were in force, however, during October.

Two and a half million adults (9% of all adults working for an employer in October) have been informed that their job is at risk. A further 28% say they may be made redundant, but had not been informed that their job is at risk.

The prospects also look gloomy for almost half of those in self-employment. Although just 4% expect to cease trading in the next six months, 16% expect their revenues to decrease a lot, and 26% expect their revenues to decrease a bit.

Given this fairly bleak outlook, it is not surprising, that nearly 16 million adults (30%) expect their household income to fall in the next six months, rising to under half (45%) of those who already have low financial resilience.

As Figure ES.4 shows, almost two-fifths (38% or 19.6m) of adults anticipate either struggling to make ends meet, seeing their debt levels increase, not being able to pay domestic bills, or not being able to keep up with their mortgage, rent or credit and loan commitments over the next six months. This figure increases to 72% among those with low financial resilience in October 2020.

Chart

Data table

Base: All UK adults (Oct 2020:22,267)

Question: FU5/6/7sum. How confident are you that you will be able to meet your mortgage payments/ rent payments/ credit and loan repayments over the next 6 months? FU8a,c. Thinking about the next 6 months, how likely is it that you will face any of the following challenges?

When asked to think about the challenges they are likely to face in the next six months, many are very worried about their financial prospects:

- 26.5 million (51%) expect to cut back on or delay non-essential spending

- 17.5 million (33%) are likely to cut back on essentials

- 8.1 million (16%) expect to take out a new credit product or borrow more on an existing one

- 5.6 million (11%) say they are likely to use a food bank

Payment deferrals

Between March and October 2020, one in six (17%) mortgage holders (3.2m) told us they took up a mortgage payment deferral. Another 14% (2.6m) of mortgage holders were considering doing so in October. Of those who took a deferral, four in ten (40%) told us they would have struggled a lot without it. Awareness of the scheme was high, with just 6% of all mortgage holders saying they might have taken a deferral, had they been aware of it.

| Adults most likely to take a mortgage payment deferral (Oct 2020) | |

|---|---|

|

Adults who were over-indebted in February |

46% |

|

Employees who were laid off or made redundant because of Covid-19 |

37% |

|

Employees who became a full-time carer or reduced their hours to care for children/ others because of Covid-19 |

31% |

|

Employees who had their hours or pay cut because of Covid-19 |

30% |

|

Adults employed on a fixed-term, temporary, zero hours, or agency staff contract in February |

26% |

|

Employees who were furloughed or put on paid leave because of Covid-19 |

26% |

|

Black, Asian and minority ethnic (BAME) adults |

23% |

|

18-34 year olds |

22% |

Female, 35-44

A fifth (19%) of adults with any credit or loan product (excluding overdrafts) told us they took a credit deferral, rising to half (49%) of those holding high-cost short-term credit such as payday loans or short-term instalment credit. Of those who took out a credit deferral, 63% took out a deferral on more than one loan. For many this support was a welcome lifeline: 32% said they would have struggled a lot more, if credit deferrals were not available.

Two-thirds (67%) of those who took up a mortgage payment deferral felt their lender was sympathetic to their circumstances. Two-fifths (41%) report their lender had contacted them to discuss their options, for example extending their deferral or extending their mortgage term to reduce future payments. The comparative statistics for those who took credit payment deferrals are 51% and 50%, respectively.

Debt advice

A total of 1.7 million people accessed debt advice between March and October 2020. Far more may need debt advice: potentially up to the 8.5 million over-indebted in October 2020. This means that 6.8 million people who might benefit from debt advice were not receiving it. Over-indebted adults tell us that the biggest barriers to accessing such services are embarrassment discussing their debts or not wanting to face dealing with the problem (35% gave this reason for not using debt advice) and lack of awareness that free services exist or whom to contact (31%).

Debt advice, however, can make a difference to those who are struggling. Around two in three (64%) debt advice users felt that their needs were understood by the adviser. For a similar proportion (62%) their debts are more manageable having spoken to an adviser.

Looking forwards, 13% of all adults (6.7m) feel that it is likely they will need debt advice in the next six months. Almost half, would like to access this advice online.

Trust in financial services

Covid-19 has had a small impact on consumers’ trust in financial services institutions. On balance, banks have seen a small improvement in being trusted: 17% of adults trust them more, while 15% trust them less. Consumers’ views of banks and mortgage lenders appear to have been shaped a great deal by their experiences of applying for mortgage payment deferrals, which, on balance have been positive.

Trust in insurance companies has suffered a net decline: 22% of adults trust insurance companies less because of Covid-19, while 11% trust them more. Over one in three (36%) believe that the insurance and protection industry did not do enough to help consumers in their response to Covid-19.

Consumers’ views are affected by their experiences. One in four (25%) have experienced at least one service-related problem with any financial services provider – including a problem getting through to them (11%) and issues using providers’ websites (9%).

Perceptions matter too. One in three (34%) adults believe that insurance companies rarely pay out, up from around one in five (22%) in February 2020. Just 4% of all adults, however, have not been able to get a refund from an insurance company or a claim has been handled poorly between March and October 2020. Of these, 21% say they trust insurance companies a little less now, and a further 14% say they trust them a lot less.

Fraud and scams

In the 12 months to February 2020, 18% of adults (9.3m) received at least one unsolicited approach involving investments, pensions and retirement planning – that might be a scam. Over a fifth (22%) say they definitely received more unsolicited approaches since the end of February than they did before Covid-19; a further 22% think this may be the case.

We asked about potential scams since the end of February related to Covid-19, such as phishing scams designed to look like they are from the Government offering Covid-19 financial support, from the NHS Test and Trace service, or from TV Licensing offering six months of free TV licence because of the pandemic. Over one-third (36%) of adults say that they have received at least one such approach.

A total of 1.4 million adults say they paid out money as a result of a Covid-19 possible scam. People with characteristics of vulnerability are more susceptible to these approaches: 12% paid out money, compared with just 1% of those with no such characteristics. Younger adults are also more susceptible: 16% of 18-24 year olds paid out money, compared with 1% of those aged 55+.

Access to cash

During Covid-19, most adults have coped well with reduced access to bank branches and ATMs and with fewer businesses accepting cash. For example:

- Around three in ten (28%) say they used online or mobile banking more regularly compared with the end of February. A further 2% say they used it for the first time since the first national lockdown began. In contrast, 46% say they visited bank or building society branches less frequently compared with the end of February.

- Around three in four (72%) who were heavily reliant on cash in February coped with reduced access to bank branches and ATMs; 73% coped with fewer businesses were accepting cash. One in seven (15%) and one in six (16%), respectively, have not coped, however.

- Over half (55%) made contactless payments more frequently in October compared with the end of February. This pattern is much the same for those who were heavily reliant on cash in February.

- One in three (34%) have provided help to a digitally excluded friend, neighbour or relative during the pandemic, to use the internet (21%), make payments online (18%), or set up online or mobile banking (11%).

Switching and shopping around

Covid-19 has increased consumer interest in shopping around for financial products. We have also seen more switching in insurance and more attention being paid to policy details, but did not capture data on this for other retail sectors. For example:

- One in three (33%) adults with insurance products are more likely to shop around in the future. For those who had never shopped around for these products previously, 10% say they are now more likely to do so.

- Three in ten (29%) adults with other financial products like current accounts, savings accounts and ISAs are more likely to shop around in the future. For those who had never shopped around for these products previously, 13% say they are now more likely to do so.

- One in six (17%) adults with insurance or protection products have switched to a new provider to lower the cost of a policy. This proportion increases to 24% for adults who were employed in February but lost their job due to Covid-19.

- One in eight (12%) adults with insurance or protection products have reviewed a policy to see what it covers; 9% have renewed a policy with changes to its terms and conditions (such as opting for higher excesses or less cover), and 8% have switched to a provider offering more appropriate cover for their needs.