This is an overview of geographical cash access coverage in the UK at the end of the second quarter (April to June) of 2023. This monitoring forms part of the FCA’s work on access to cash.

1. Introduction

Each quarter, with the Payment Systems Regulator (PSR), we gather and update data on access to cash. This captures the locations of cash access points and other relevant information such as temporary closures, opening hours, and accessibility. This data covers brick-and-mortar, mobile bank, and building society branches, automated teller machines (ATMs), and the Post Office network. We supplement this information with annual data on cashback locations.

This analysis provides insights on the proportion of the population that lives within a range of distances of various types of cash access point. We measure distances as the crow flies (see note 1), consistent with the approaches adopted by LINK and the Post Office, relative to residential addresses (see note 2).

We estimate that for access to larger banks and building societies providing Personal Current Accounts (PCA) and Post Office: all branches, including mobile bank branches:

- 97.4% of the UK urban population are currently within 1 mile of a free-to-use cash access point offering deposits

- 98.2% of the UK rural population are currently within 3 miles of a free-to-use cash access point offering deposits

We estimate that for access to any bank, building society, Post Office branch, or any free ATM:

- 99.3% of the UK urban population are currently within 1 mile of a free-to-use cash access point offering withdrawals

- 98.6% of the UK rural population are currently within 3 miles of a free-to-use cash access point offering withdrawals

Consumers and businesses can deposit and withdraw cash through a wide variety of channels. As such, for the UK as a whole, estimates of coverage across all facilities (brick-and-mortar and mobile bank and building society branches, ATMs, and post offices) at 1 mile and 3 miles have seen little clear change since 2023 Q1, despite the number of bank branch closures. In terms of the places that provide cash services, we found:

- The number of brick-and-mortar branches of the larger bank and building societies providing cash services fell by 210 branches, a decrease of 4.7%. This particularly affected the east and north east of England and Yorkshire & The Humber.

- The number of post offices was stable.

Our analysis of other access characteristics finds that during this period:

- There was an increase (2%) in the number of larger banks and building societies (type A) opening on Saturdays between 9am and 12pm.

- There was an increase (2.5%) in the number of larger banks and building societies (type A) opening on weekdays between 3pm and 4.30pm.

- There was an increase (1.3-1.8%) in the number of smaller banks and building societies (type B) opening on weekdays between 9am and 4pm.

- Post Offices showed a small trend of branches opening progressively later in the afternoons, Monday to Saturday, with an increase of 0.6% of branches open at 7pm.

- Temporary closures of type A (brick-and-mortar branches of a larger PCA provider) showed a decrease of 20% from 2022 Q4 [see note 11]. The number of branches closed for one day or more fell from 7.4% in 2023 Q1 to 5.5% in 2023 Q2. We cannot get reliable results for type B (smaller branches) due to a high proportion of branches not returning data.

2. Coverage

The data comprises 67,137 known UK cash access points and 487,143 cashback locations. Table 1 shows numbers by region for 8 types of access point (see notes 3, 4, and 5):

- Types A and B are brick-and-mortar bank and building society branches provided by (A) larger PCA providers and (B) all other banks and building societies, respectively.

Type B branches may offer more limited deposit and withdrawal services compared to type A branches. For example, a building society that specialises in mortgages or savings accounts.

- Mobile bank branches (measured by stops) are a separate type (D).

- Post Office branches are subdivided into mobile/ outreach branches (type E) and all other Post Office branches (type C). The outreach branches are brick-and-mortar but are more similar to mobile branches being typically open for a small number of hours or on selected days of the week. For example, these include limited time to serve access points in community buildings in rural locations. For this reason, we group the mobile and outreach branches together.

- ATMs are subdivided into free-to-use (type F) and pay-to-use (type G). These figures were last updated in 2022.

- Cashback locations (type H) are all the unique locations where a cashback transaction took place in 2022.

Table 1: Number of cash access points by type and geographical area

| Country/ geographical area | England | Northern Ireland | Scotland | Wales | UK Total | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Type | Description | East Midlands | East of England | London | North East | North West | South East | South West | West Midlands | Yorkshire and The Humber | ||||

| A | Larger banks and building societies providing PCA (brick-and-mortar branches) | 262 | 395 | 572 | 164 | 428 | 597 | 363 | 365 | 292 | 138 | 446 | 243 | 4,265 |

| B | All other banks and building societies (brick-and-mortar branches) | 87 | 66 | 53 | 49 | 94 | 68 | 76 | 126 | 98 | 31 | 36 | 105 | 889 |

| C | Post Office branches excluding mobile/ outreach | 735 | 1,007 | 724 | 400 | 981 | 1,254 | 993 | 802 | 811 | 464 | 1,052 | 684 | 9,907 |

| D | Mobile bank branches | 24 | 22 | 5 | 27 | 59 | 95 | 10 | 10 | 13 | 416 | 97 | 778 | |

| E | Mobile/ outreach Post Office branches | 138 | 189 | 95 | 150 | 138 | 265 | 111 | 150 | 29 | 259 | 261 | 1,785 | |

| F | Free-to-use ATMs | 2,712 | 3,229 | 5,179 | 1,720 | 4,288 | 4,745 | 2,944 | 3,395 | 3,334 | 1,417 | 3,903 | 1,860 | 38,726 |

| G | Pay-to-use ATMs | 648 | 850 | 1,668 | 529 | 1,465 | 1,091 | 683 | 1,176 | 781 | 325 | 978 | 593 | 10,787 |

| H | Cashback locations | 33,848 | 43,550 | 67,628 | 17,360 | 53,496 | 69,142 | 46,551 | 36,770 | 39,134 | 13,952 | 42,549 | 23,163 | 487,143 |

| All sources excluding cashback | 4,606 | 5,758 | 8,196 | 2,962 | 7,433 | 7,952 | 5,419 | 5,985 | 5,476 | 2,417 | 7,090 | 3,843 | 67,137 | |

| All sources including cashback | 38,454 | 49,308 | 75,824 | 20,322 | 60,929 | 77,094 | 51,970 | 42,755 | 44,610 | 16,369 | 49,639 | 27,006 | 554,280 | |

We have analysed coverage for 14 groups of cash access points which we define in Table 2. The groups are constructed by combining the cash access point types and cashback locations:

- group 1 includes type A (larger banks and building societies providing PCA) access points only

- group 2 adds the non-mobile/outreach Post Office network

- group 3 includes all brick-and-mortar (except type B) and mobile/outreach bank, building society, and Post Office branches, representing all known locations where customers can access banking services beyond cash withdrawals or deposits

- groups 4 and 5 include the same cash access point types as Group 3, as well as all free-to-use ATMs and all ATMs respectively

- group 6 includes type B branches and contains all free-to-use access points

- group 7 includes all 67,137 known cash access points

- groups 8 and 9 focus on access to ATMs, for free-to-use and all ATMs respectively

- groups 10, 11, and 12 combine free-to-use access points, all access points and all ATMs respectively with cashback locations

- groups 13 and 14 focus on access to the Post Office network distinguishing between non-mobile/outreach branches and all branches

Due to substitutability, as outlined above, type B branches are only included in groups 6, 7, 10, and 11.

Table 2: Groupings of cash access points

| Group | Description | Cash access point types included | Number of entries | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| A | B | C | D | E | F | G | H | |||

| 1 | Larger banks and building societies providing PCA: brick-and-mortar branches | x | 4,265 | |||||||

| 2 | Larger banks and building societies providing PCA and Post Office: brick-and-mortar branches | x | x | 14,172 | ||||||

| 3 | Larger banks and building societies providing PCA, and Post Office: all branches, including mobile | x | x | x | x | 16,735 | ||||

| 4 | Post Office, larger banks and building societies providing PCA (all branches), and free-to-use ATMs | x | x | x | x | x | 55,461 | |||

| 5 | Post Office, larger banks and building societies providing PCA (all branches), and all ATMs | x | x | x | x | x | x | 66,248 | ||

| 6 | All free-to-use cash access points (excluding cashback) | x | x | x | x | x | x | 56,350 | ||

| 7 | All cash access points (excluding cashback) | x | x | x | x | x | x | x | 67,137 | |

| 8 | Free-to-use ATMs | x | 38,726 | |||||||

| 9 | All ATMs | x | x | 49,513 | ||||||

| 10 | All free-to-use cash access points and cashback locations | x | x | x | x | x | x | x | 543,493 | |

| 11 | All cash access points and cashback locations | x | x | x | x | x | x | x | x | 554,280 |

| 12 | All ATMs and cashback locations | x | x | x | 536,656 | |||||

| 13 | Post Office branches excluding outreach and mobile | x | 9,907 | |||||||

| 14 | All Post Office branches | x | x | 11,692 | ||||||

On this web page we provide highlights of coverage in Table 3. We present data for groups 3 and 6 as proxies for cash deposit and free cash withdrawal access for consumers. We provide these figures for Great Britain, Northern Ireland and the UK as a whole split by overall, rural and urban at distances of 1 mile and 3 miles.

Table 3: Percentages of the UK population that have access to a source of cash within a given distance as of 2023 Q2 (groups 3 and 6)

Group 3: Larger banks and building societies providing PCA and Post Office: all branches, including mobile 2023 Q2

| Region | Rural / Urban | Population, 000's | 2km | 5km | 1 mile | 3 miles |

|---|---|---|---|---|---|---|

| UK | Overall | 67071.7 | 95 | 99.7 | 92.6 | 99.6 |

| UK | Rural | 12046.4 | 77 | 98.5 | 70.7 | 98.2 |

| UK | Urban | 55025.3 | 98.9 | 99.9 | 97.4 | 99.9 |

| GB | Overall | 65176.2 | 95.3 | 99.7 | 93 | 99.7 |

| GB | Rural | 11337.1 | 78.1 | 98.6 | 71.9 | 98.3 |

| GB | Urban | 53839.1 | 98.9 | 99.9 | 97.4 | 99.9 |

| NI | Overall | 1895.5 | 83.8 | 98.7 | 79.6 | 98.5 |

| NI | Rural | 709.3 | 58.7 | 96.6 | 51.5 | 96 |

| NI | Urban | 1186.2 | 98.9 | 100 | 96.4 | 100 |

Group 6: All free-to-use cash access points (excluding cashback) 2023 Q2

| Region | Rural / Urban | Population, 000's | 2km | 5km | 1 mile | 3 miles |

|---|---|---|---|---|---|---|

| UK | Overall | 67071.7 | 96.3 | 99.8 | 95 | 99.7 |

| UK | Rural | 12046.4 | 81.2 | 98.8 | 75.7 | 98.6 |

| UK | Urban | 55025.3 | 99.6 | 100 | 99.3 | 99.9 |

| GB | Overall | 65176.2 | 96.6 | 99.8 | 95.4 | 99.7 |

| GB | Rural | 11337.1 | 82.3 | 98.9 | 76.9 | 98.7 |

| GB | Urban | 53839.1 | 99.6 | 100 | 99.3 | 99.9 |

| NI | Overall | 1895.5 | 86.4 | 99.2 | 83.3 | 99.1 |

| NI | Rural | 709.3 | 64.1 | 97.9 | 56.6 | 97.5 |

| NI | Urban | 1186.2 | 99.7 | 100 | 99.3 | 100 |

Estimated percentages of the UK population living within a given distance from a cash access point for all groups 1-14 can be downloaded via the link below (see notes 6, 7, and 8).

We give the estimates for the UK regions and devolved nations separately, as well as for England and the UK overall. Estimates for rural and urban areas are also given (see note 9).

The distances considered are 1, 2, 3, 5, and 10 miles (approximately 1.6, 3.2, 4.8, 8.0 and 16 km, respectively).

Download Table 3 data (xlsx)

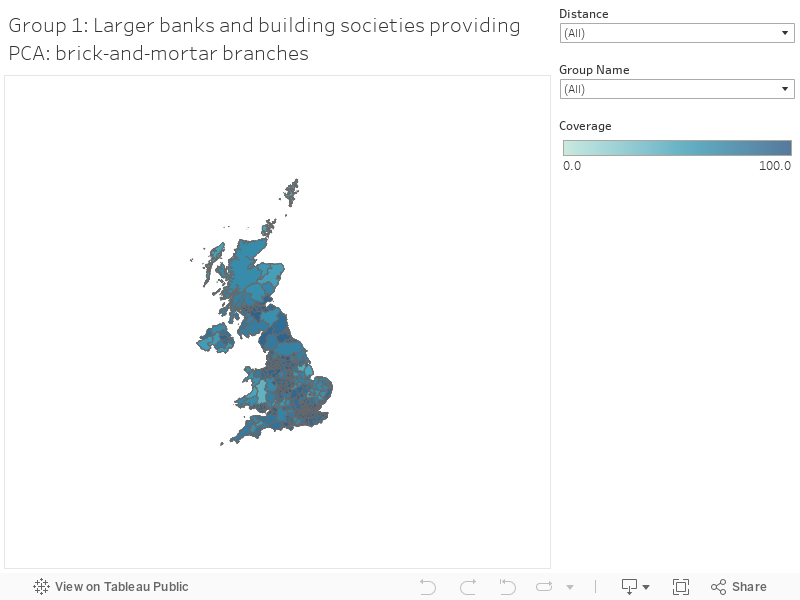

Figure 1 shows the coverage areas underlying the population estimates in Table 3. As in Table 3, the cash access points considered are those in groups 1-14. In each case the areas shown are those without access to a source of cash within 1, 2, 3, 5 and 10 miles. The interactive tooltips show percentages of the Local Authority District population that have access to a source of cash within the above range of distances.

Download underlying data for Figure 1 maps (XLSX)

Figure 1: Access to cash coverage in the UK in 2023 Q2

3. Other insights

3.1. Temporary closures

We cannot give precise figures for temporary closures because a high proportion of branches did not provide this information. But there has been a decrease in the overall number of days closed across type A (large PCA providers) since 2023 Q1. Of type A branches that did provide this information (84%) there were 5.5% that were temporarily closed for at least one day, which is a decrease on 2023 Q1 (7.4%).

We do not have equivalent information for Post Office branches.

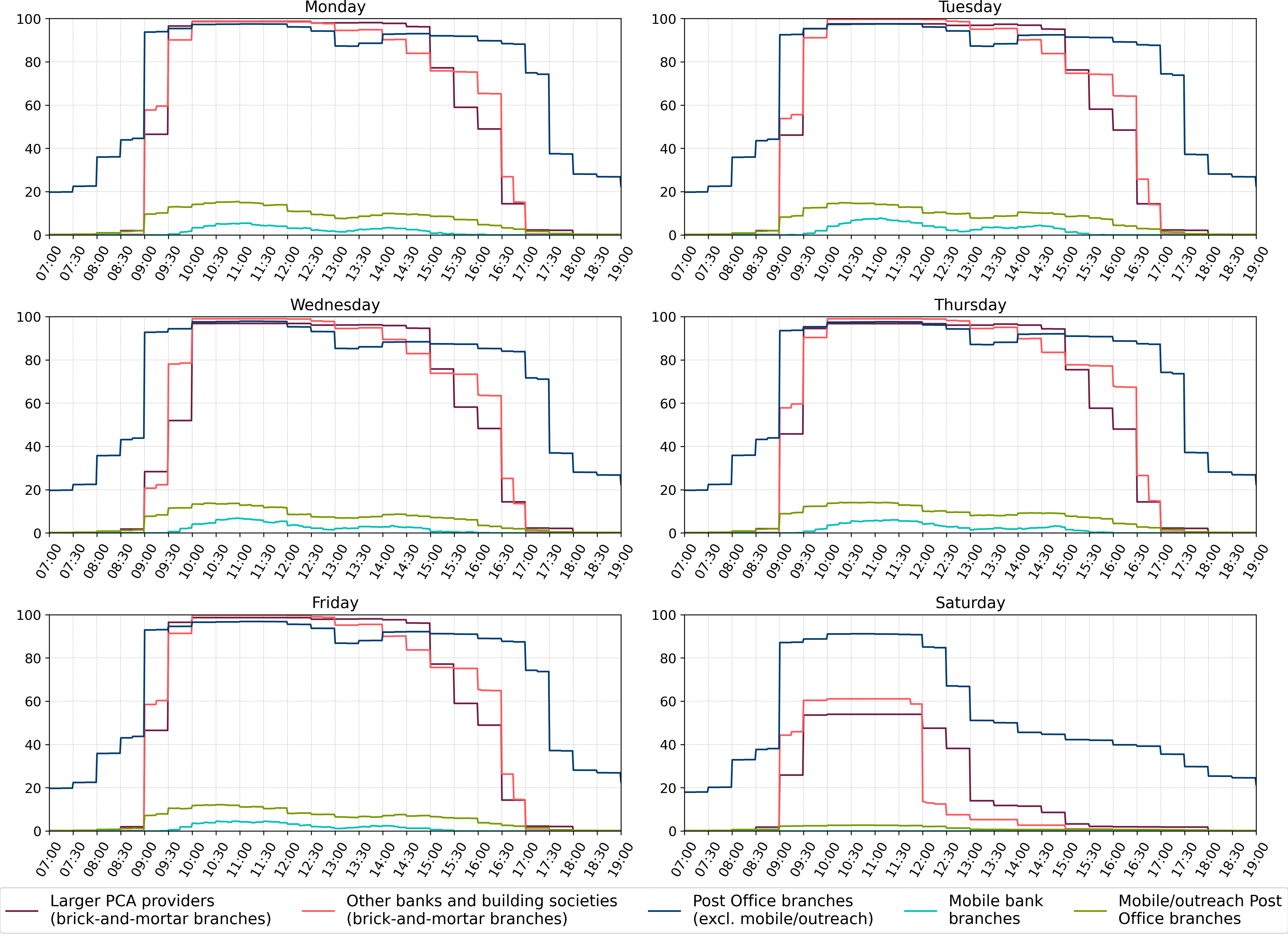

3.2. Opening hours

While external and stand-alone ATMs are always accessible, in-branch cash withdrawals and deposits and other banking services are only available during branch opening hours.

Figure 2 shows the percentages of branches open at a given time between 7am and 7pm, Monday to Saturday (see note 10), by branch types defined in Table 1.

Figure 2 Percentages of branches open at a given time by branch type

3.3. Accessibility

For some consumers, being able to use branch services depends on accessibility.

Table 4 shows percentages of branches that are wheelchair accessible, have step-free access and/or have a hearing/induction loop available for the 3 types of bank and building society branches (see note 10). The step-free access characteristic is not applicable to mobile branches (see note 11).

Of the brick-and-mortar bank and building society branches, 65.2% of type A (larger PCA providers) and 53.1% of type B (other) branches have all 3 features. Excluding the branches for which some values are unreported, these percentages become 91.2% and 69.3% respectively.

Table 4: Percentages of branches with common accessibility characteristics by branch type

| Wheelchair accessible | Has step-free access | Has hearing/ induction loop available | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Access point type | Sample | Yes | No | Unreported | Yes | No | Unreported | Yes | No | Unreported |

| A: Larger banks and building societies providing PCA (brick-and-mortar branches) | All data | 94.4 | 5.6 | - | 68.7 | 2.8 | 28.5 | 99.2 | 0.8 | - |

| Excluding unreported | 94.4 | 5.6 | x | 96.1 | 3.9 | x | 99.2 | 0.8 | x | |

| B: All other banks and building societies (brick-and-mortar branches) | All data | 78.4 | 5.7 | 15.9 | 69.0 | 7.6 | 23.4 | 64.3 | 21.4 | 14.3 |

| Excluding unreported | 93.2 | 6.8 | x | 90.0 | 10.0 | x | 75.1 | 24.9 | x | |

| D: Mobile bank branches | All data | 77.4 | 22.6 | - | - | 100.0 | - | 100.0 | - | - |

| Excluding unreported | 77.4 | 22.6 | x | - | 100.0 | x | 100.0 | - | x | |

4. Attributions

In addition to the data collected from banks, building societies, and the Post Office, the analysis uses other open data and data licensed under the Public Sector Geospatial Agreement.

- ATM data © LINK Scheme Ltd, LINK Network Members, and licensors copyright and database right 2023.

- Contains OS data © Crown copyright and database right 2023.

- Contains NRS data © Crown copyright and database right 2022.

- Contains NISRA data © Crown copyright and database right 2021.

- Contains National Statistics data © Crown copyright and database rights 2021/2022/2023.

- Contains Royal Mail data © Royal Mail copyright and database right 2023.

- Office for National Statistics licensed under the Open Government Licence v.3.0.

- Contains public sector information licensed under the Open Government Licence v3.0.

- This product contains data created and maintained by Scottish Local Government.